Q4 Model update V3.2

2035 Vehicle to Grid EV Assumptions

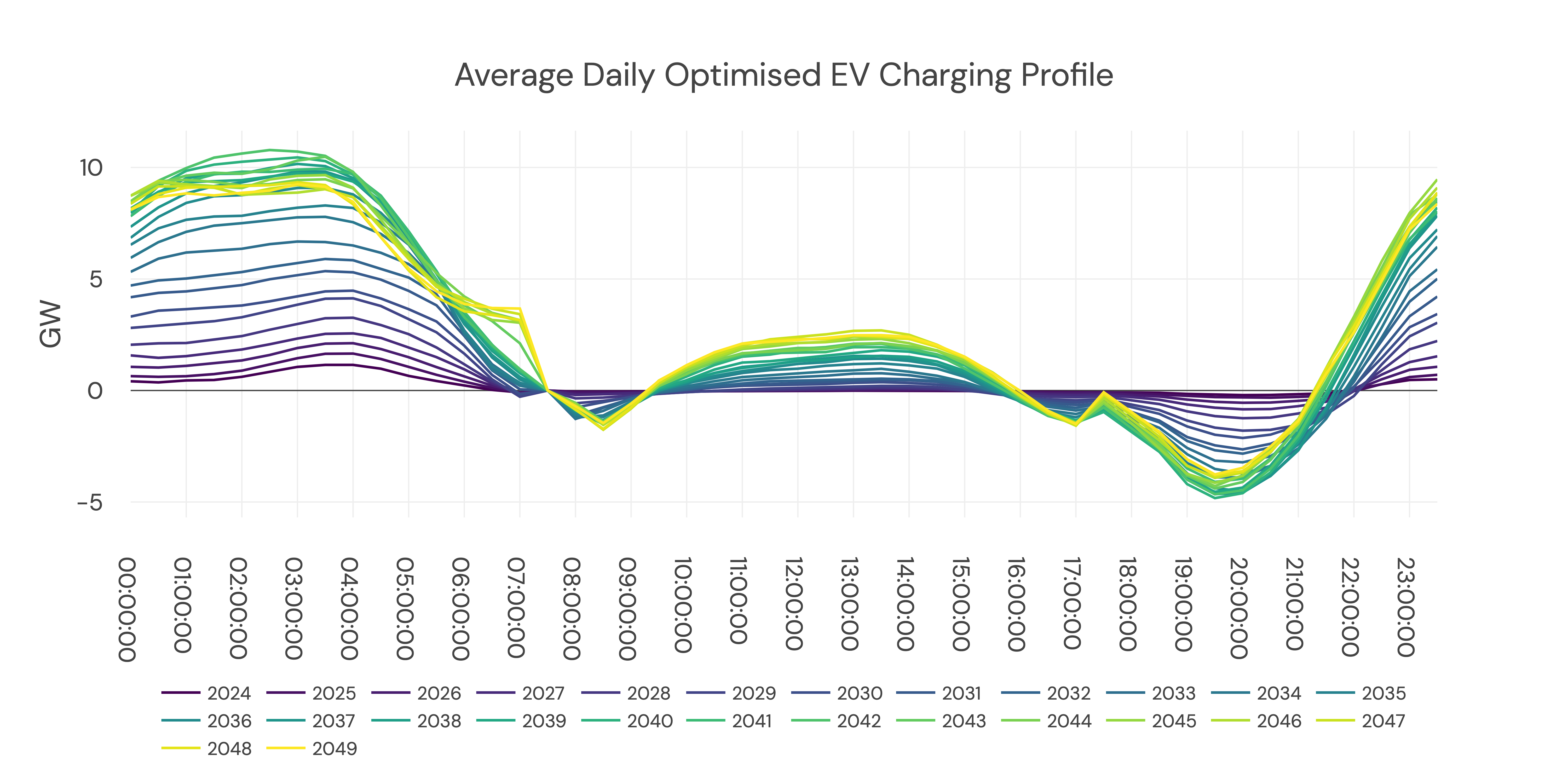

There was a lot of interest around our Vehicle to Grid modelling. Here's a brief summary of our assumptions, with a focus on 2035:

We assume that there are 17 million BEVs in GB in 2035. Of these, we assume that 17% are capable of vehicle-to-grid discharge. We assume a 4kW charger per Vehicle to Grid enabled EV, with 66% of those being available to charge and discharge overnight. This equates to a maximum discharge of 7.9 GW in 2035. However, discharging at this power is rare in our model - the average evening vehicle to grid discharge peak is <5GW for all years in our forecast, as shown below:

We assume that V2G discharge is traded in the day ahead market.

For more information on our EV assumptions, including our assumptions for smart charging and non-price responsive EVs, head to the EV section of our methodology.

Flexibility Beyond Domestic EVs and BESS

We had a few questions about our assumptions for flexibility of the power system outside of BESS and residential EVs (e.g., non-domestic EVs, electric heating, I&C demand).

We model flexibility in residential EVs, BESS, pumped storage and other storage (compressed air etc.) fleet dispatch model (more on this model here). Outside of these technologies, we model flexibility by including demand side response (DSR) in our generation stack.

Demand side response (DSR) is priced at £250/MWh, £500/MWh, and £1500/MWh. It sits near the top of the generation stack, with loss of load pricing at £6,000/MWh above it.

Fleet cannibalisation

Does the BESS storage cannibalisation ratio include the impact of EVs? Also, what does the ratio look like from a GWh POV?

No we only include stationary BESS in the cannibalisation ratio. The impact of EVs is to change the shape of demand and prices, against which the BESS fleet dispatches. EVs reduce price spreads, which the stationary BESS fleet further cannibalise.

How do you explain that there is no canibalisation ratio under 20 GW of BESS ?

We assume that the BESS fleet is cleverly optimized and does not all charge or discharge at once. If the entire BESS fleet charged simultaneously during a predicted low price period, demand and price would increase, resulting in high charging costs for the fleet. So we spread out fleet storage charge and discharge to prevent it from adversely affecting prices. Additionally, a proportion of the fleet will be providing ancillary services and will be unavailable for wholesale trading.

Both of these factors mean that the volume of BESS power traded in the wholesale market will be much lower than the fleet’s nameplate capacity. We find that below 20 GW due to participation in ancillary services and the charge and discharge of the BESS fleet being spread out, we do not see any wholesale spread cannibalization.

Other questions

How many balancing zones do you model?

More details on how location impacts revenues in our model can be found on this page. We model the following key transmission boundaries when calculating volumes in each region: B2, B4, B5, B6, B7a, EC5, LE1, and B14,

Is there a benefit for batteries above 300 MW to split into separate BMUs

Ramp rate restrictions apply at the level of the grid supply point, so batteries that split into separate BMUs still face these restrictions.

Updated 9 months ago