Optimising battery dispatch in intraday markets

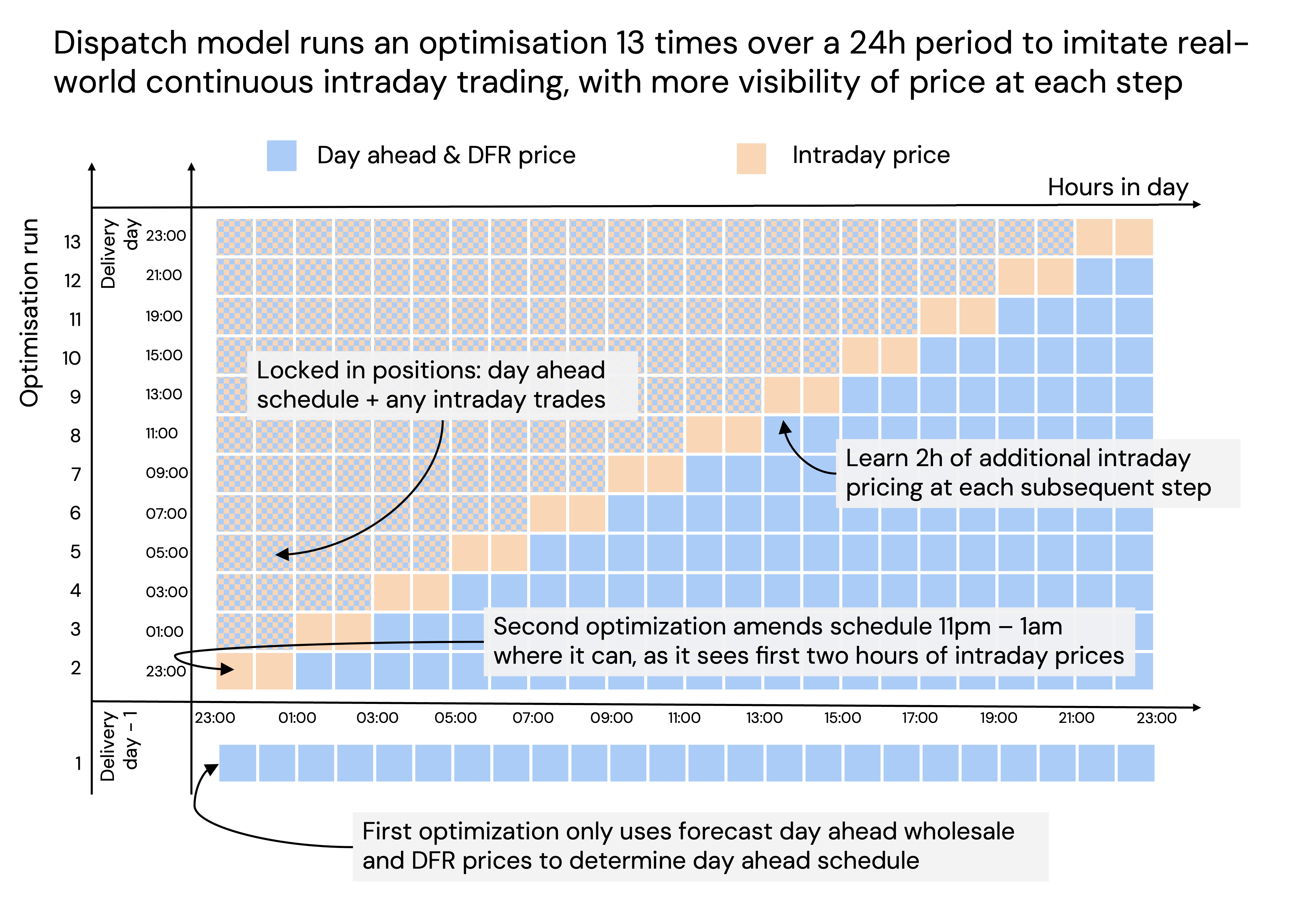

A schematic of how we use multiple optimisations to model the intraday revenues as more prices are known is shown below.

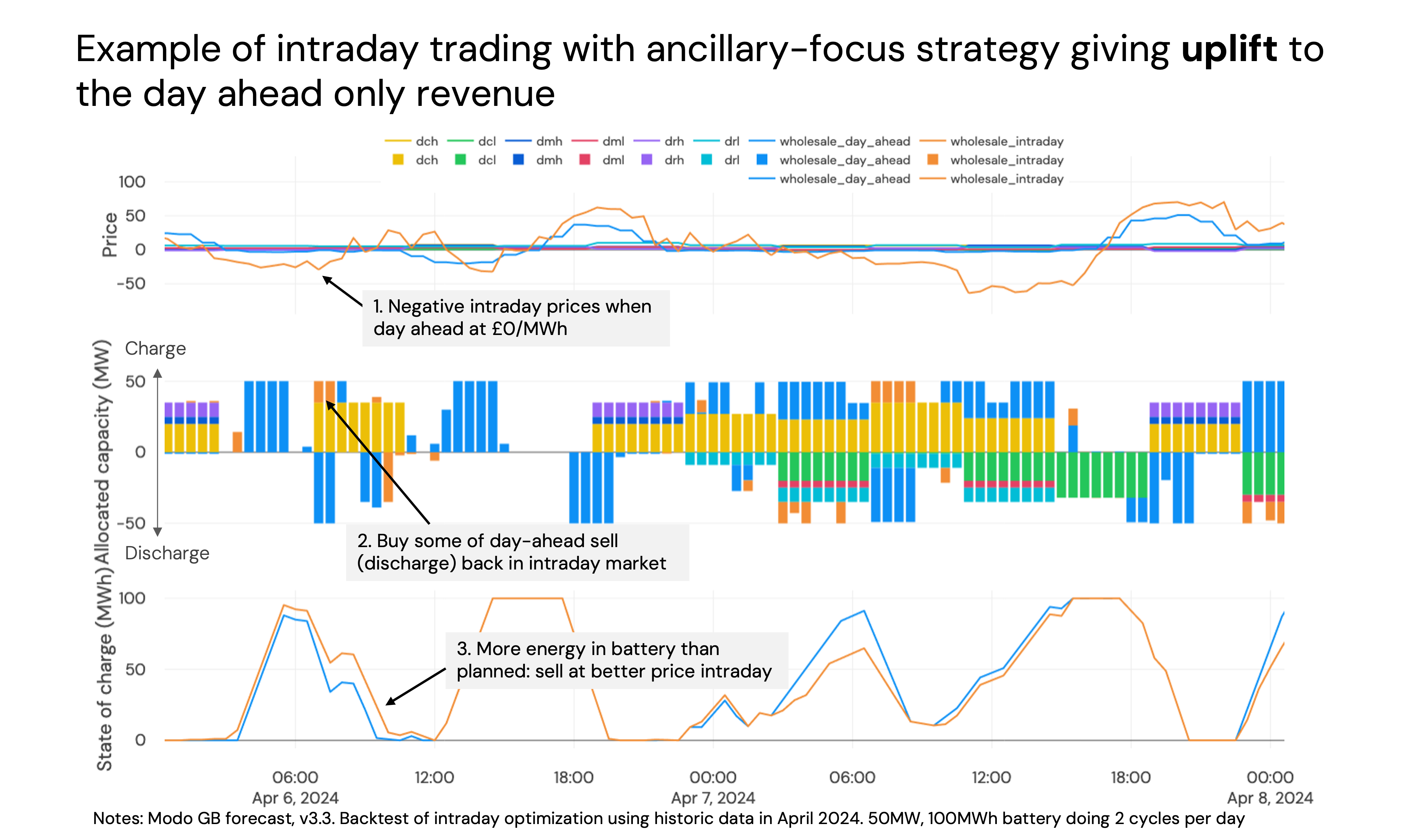

How does the intraday dispatch modify the day ahead position?

Sometimes more revenue can be made by re-optimising intraday

If there is headroom or footroom available after the day-ahead optimisation, when an intraday opportunity presents itself, wholesale positions can be adjusted to bring in additional intraday revenues. The example below, focussing on the 6th April, gives an example of this.

A 50MWh discharge (or sell order) for 7am is placed in the day-ahead market, the day before delivery. 2h before delivery, that discharge is adjusted to take advantage of some negative intraday prices - there is a spread between the day ahead and intraday price at this time, which the battery has capacity to take advantage of. So, it buys back 10MWh in intraday markets, at a profit.

The additional energy that remains in the battery is also then sold later on at a higher price than would have been achieved in the day-ahead market.

This is an example of asset-backed non-physical trading.

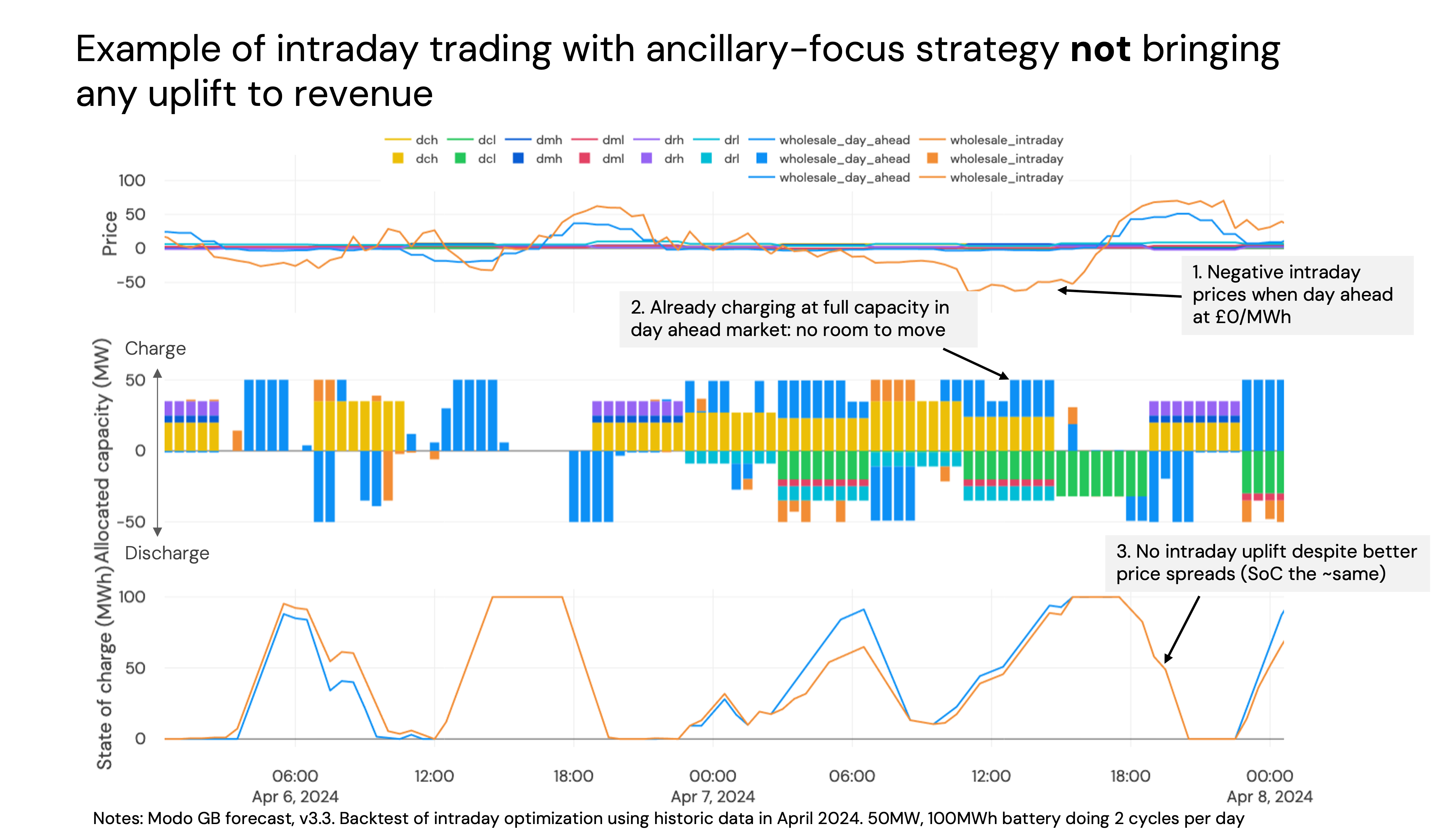

But, sometimes the day ahead position means there is no revenue uplift, even when intraday spreads are better than those day ahead

Intraday prices are not known more than 2 hours ahead of time, and when we choose what to do the day ahead stage, we don't specifically leave any battery capacity for intraday trading. I.e., the day-ahead optimisation does not consider any potential revenue uplift that could be available intraday when making decisions. This means that sometimes opportunities will be left on the table, as in the example highlighted below.

Again, on the evening of the 7th April, intraday prices were more negative than day-ahead prices. However, during this time period, the battery was already using all its charging capacity in other markets. It had a dynamic containment high contract with 25MW of it's 50MW capacity, and a 25MW charge action with the rest of it (i.e. a buy order in the day-ahead market). There is no additional MW available within the battery to take advantage of the negative intraday prices, so there is no revenue uplift here - despite better prices intraday!

This may raise a question over why we chose to set up the optimisation like this, and not, for example, leave some headroom and footroom for intraday trading. More detail on this here.

Updated 9 months ago