Intraday prices

How we build an intraday price forecast

Modo now produces an intraday price forecast as well as a Day-Ahead price forecast.

In v3.3 of the GB forecast, we built a new model to produce these intraday prices. Now, in any one day of the forecast horizon (to 2050), the Modo forecast produces both a day-ahead price and an intraday price in each half-hour period.

Find out how these prices are used to get intraday battery revenues here.

Modelling intraday prices

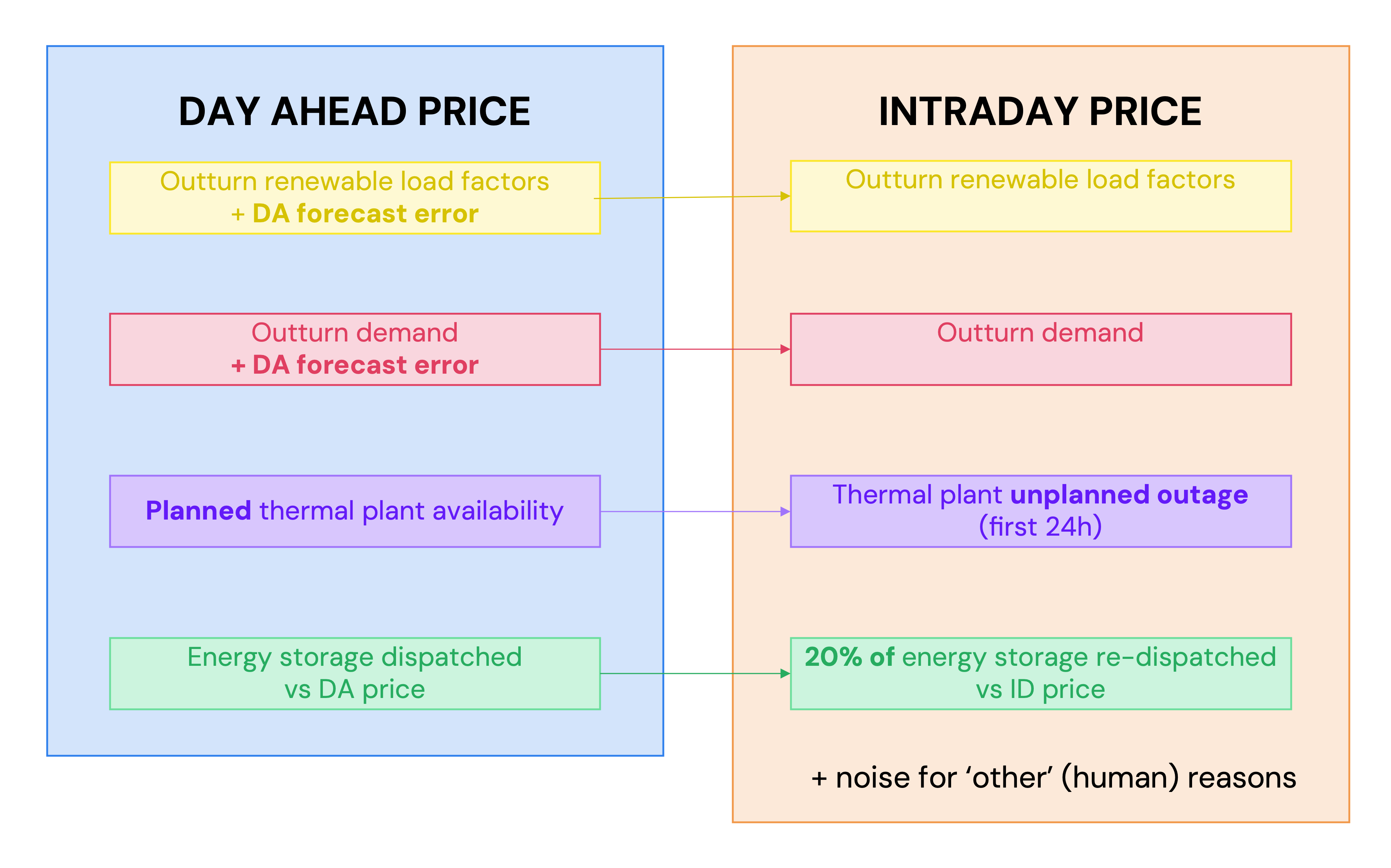

Evolution of forecasts of renewables & outages impact Day Ahead and Intraday prices

The Day-Ahead price of electricity is informed by forecasts for demand, wind and solar generation, and plant availability. These forecasts are critical to building the supply stack to meet demand from one half-hour to the next -and setting power prices.

As time progresses from the closure of the day-ahead market to delivery, forecasts for each of these variables evolve into the outturn values. The intraday markets allow power to be bought and sold in response to these changing forecasts until 20 minutes before the delivery window starts.

While the Day-Ahead price and Intraday price are highly correlated, the evolution of these forecasts (along with human behaviours) causes intraday prices to diverge from their day-ahead reference point. These price changes represent an opportunity for storage to optimize against.

- More information on how we model demand, wind and solar generation forecast errors is here

- Information on modelling plant outages is here

- Information on how we model 'other' things that can change intraday prices, like human behaviour, is here

Modo's intraday forecast represents the EPEX Continuous Intraday market reference price of products traded at half-hourly granularity, or RPD HH. The actual data of EPEX RPD HH is available via our API here.

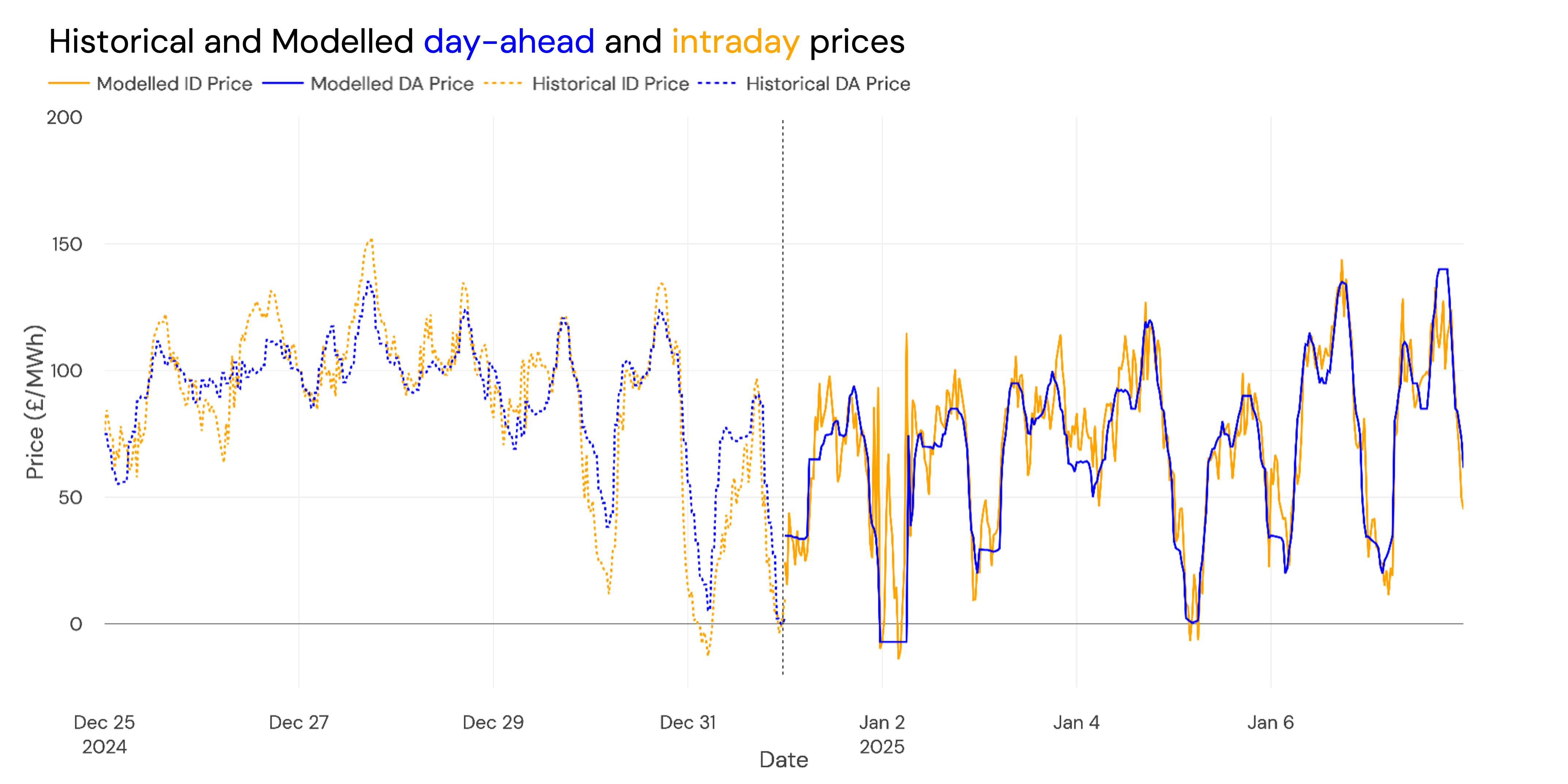

An example of intraday prices in reality and our model is shown below

Backtest of intraday prices

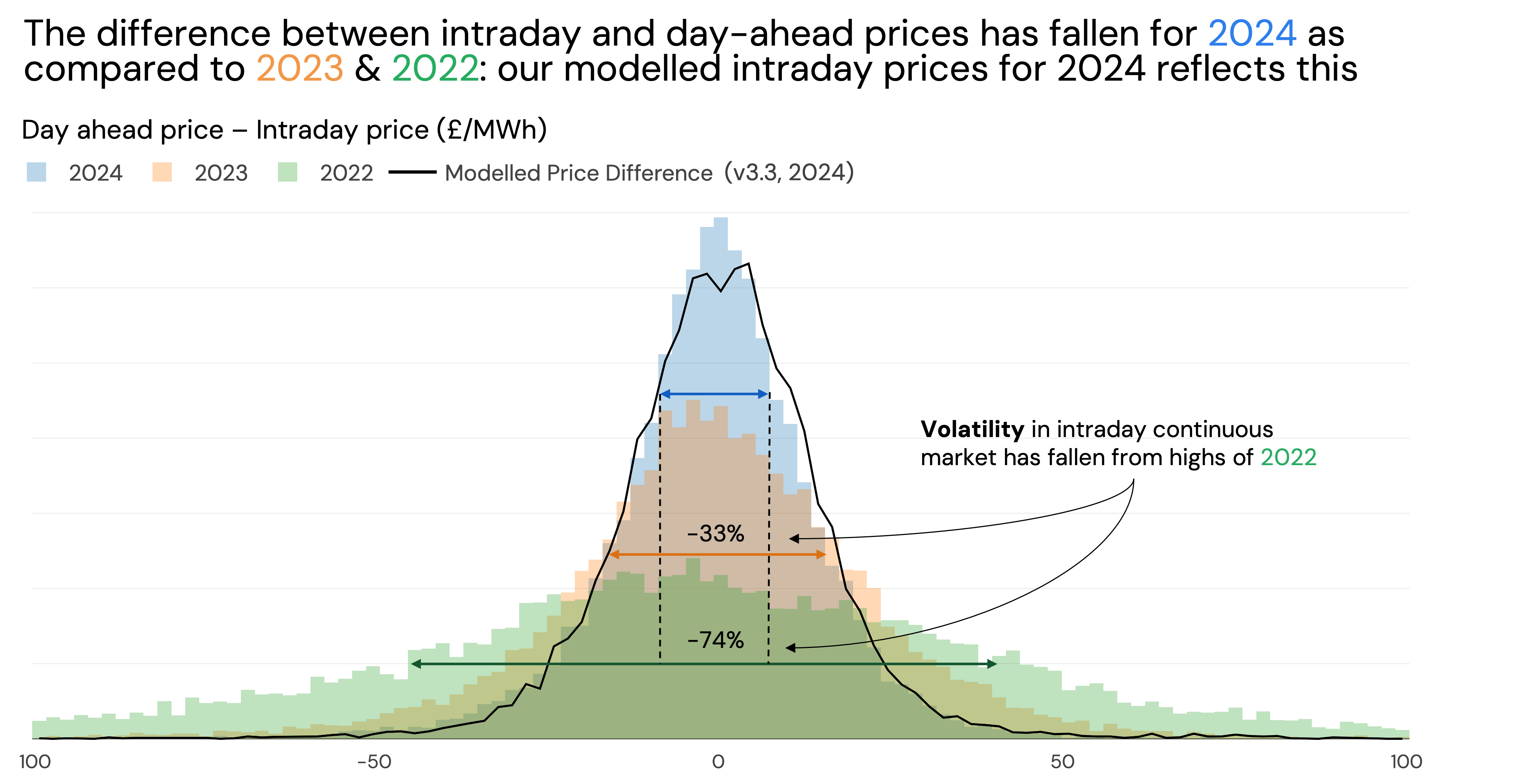

We look at how the forecast of intraday prices compared to actual intraday prices in 2024. The blue shaded region below shows the difference between day-ahead (N2EX) and intraday (EPEX RPD HH) prices in real data in 2024 and the black line is the forecast difference for the same time range.

What's interesting is that volatility in intraday markets has fallen across the last few years; in 2024, intraday prices were closer to day-ahead prices than in 2022.

While wider geopolitics, of course, influenced the volatility in previous years, possible reasons for less volatility in 2024 are more interconnection to European neighbours smoothing prices and more volume traded on the intraday continuous markets (particularly algorithmic trading—though its not clear whether bots would increase or decrease volatility!)

What it does mean is that using an intraday uplift for a long-term revenue curve based on anything but the latest data could falsely inflate those intraday revenues. More on this here.

Updated 9 months ago