Large >300MW BESS sites

We do not recommend using our Central curve to forecast (very) large BESS sites.

A battery of 50MW is a different proposition to one of 1000MW, so we have an alternate way of producing curves for these assets.

Essentially, we expect a lower £/MW/year.

You can access a forecast for a large asset via a single custom run, submitting the details of the single large site, which we will break down as detailed below.

If you intend to break the large asset into several BMUs connected at the same Grid Supply Point, please submit the whole site to avoid inaccurate revenue curves.

What does large mean?

There is a ramp rate restriction on any single generator site at a Grid Supply Point that kicks in at 300MW. For this reason, we determine that 'large' is anything over 300 MW (BC.1.A.1.1. of the Balancing Code, here).

How many 'large' sites are operational now?

No batteries currently exceed this 300MW threshold.

There is one 200MW battery active, Zenobe's Blackhillock (400MWh).

Currently, there are 4 BESS sites operational with a size of 100MW each:

- Dollymans, which exists as a single BM unit of 100MW (100MWh)

- Minety, which is split into Minety Lower and Minety Upper, both 50MW (56MWh)

- Capenhurst, which is split into 4 x 25MW (26MWh) units

- In October 2024, Lakeside became operational, 100MW (200MWh).

Stratera's Thurrock (300MW, 600MWh) is also due online soon.

However, in 2025 and 2026, we expect more larger assets to come online, and the Modo buildout report includes several projects >300MW.

How might a site > 300MW be operated?

Big BESS sites are likely to be split into several sub-units – a 1GW BESS might (for example) be split into 6, with each unit doing something different.

- One (or more) subunits might be contracted under longer-term contracts or tolled, hedging some of the risk and the owner may take a lower £/MW as a result. However, it will still be operated in the spot markets by the organisation that rented the asset - receiving a mix of the standard revenue streams.

- Units will be exposed to merchant revenues. These revenues are very slightly lower due to the ramp rate restrictions on such a unit as per the Balancing & Settlement Code (BC.1.A.1.1.) - for a 500MW site, we expect this to be of order 0.5%.

- Parts of one of the units might hold an ancillary service contract. There is (as of October 2024) a limit on the amount of frequency response a single unit can delivery: 50MW for DR and DM, and 100MW for DC. We expect all three to be at a 100MW limit by the end of the year. Of course, these markets are already fully saturated - we would not forecast any sub-unit to be delivering these services at its full capacity.

- For usage in the Balancing Mechanism, with the Open Balancing Platform, large sites are likely to be dispatched at the same rate as smaller sites. However, the amount of energy used is not likely to be the full capacity of the system, as the control room won’t always need 500MW+. More on this below.

Our central forecast does not capture all of these nuances which are specific to assets >300MW.

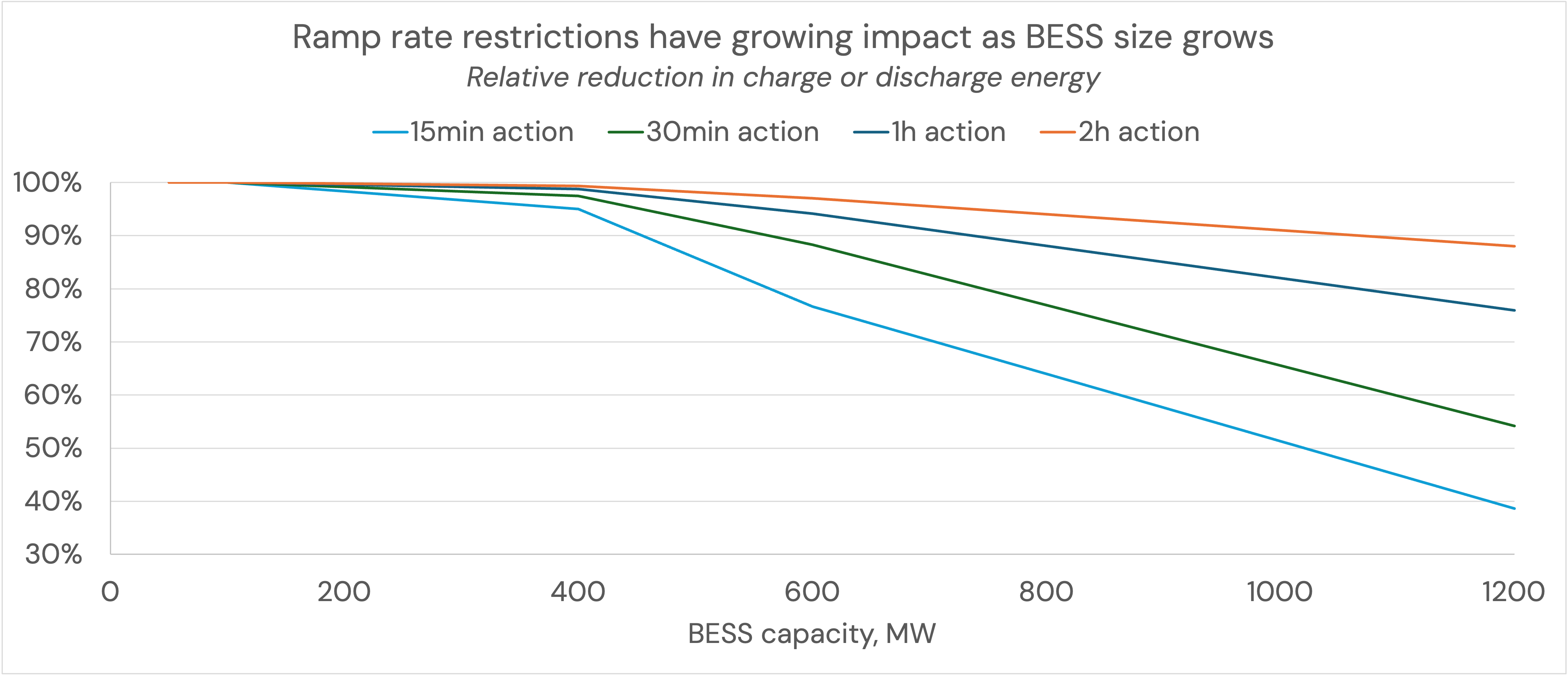

What impact do these ramp rate restrictions have?

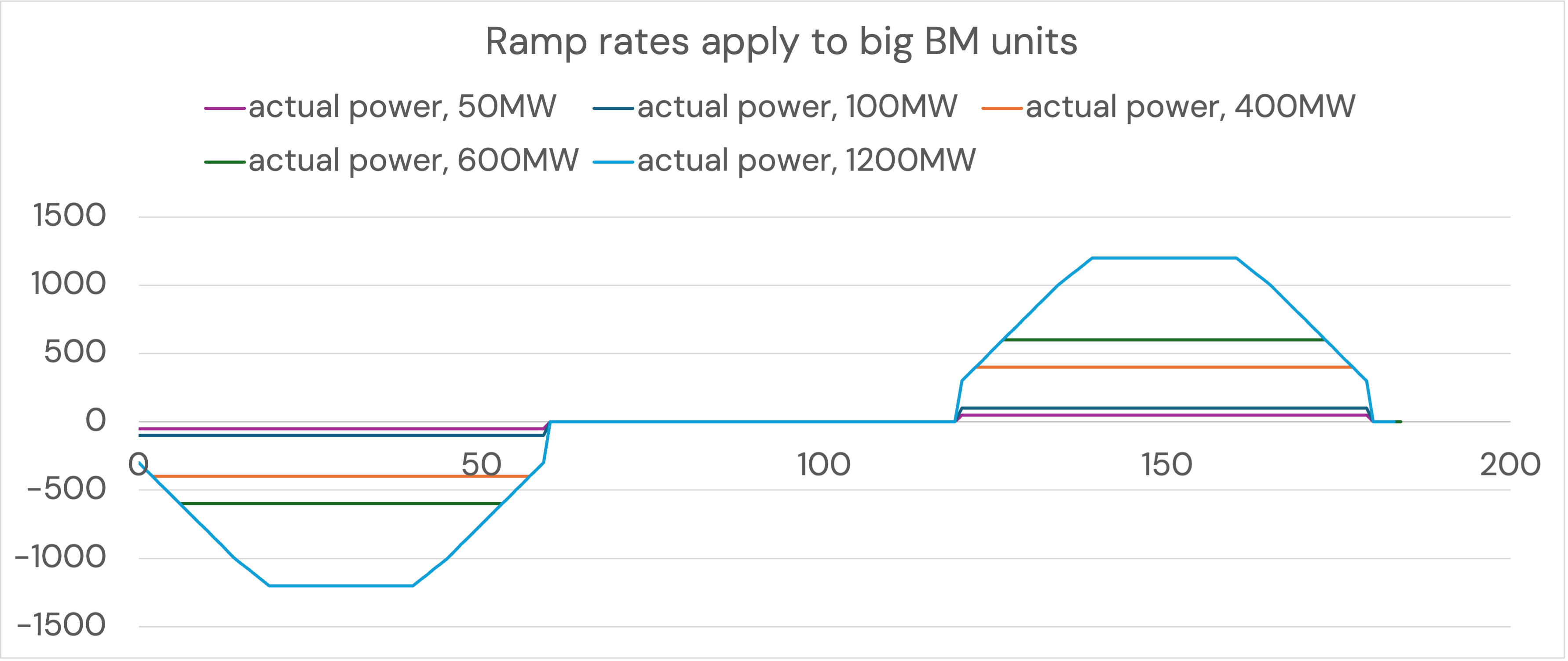

The amount of energy that can be charged and discharged is restricted, depending on the duration of the action. An example of a 1-hour charge and discharge is shown below, for different sized BM units. The longer the duration of charge or discharge, the lower the impact.

The model considers ramp rates. Optimisation profiles adjust to produce longer (smoother) charges and discharges, meaning the impact is minor.

These ramp rates do not apply in the Balancing Mechanism.

Modeling the revenue stack of assets > 300MW

In v3.2 of the Modo forecast, we have modified the dispatch model to account for the ramp rate restrictions shown above. We also cap any ancillary service contact to 100MW.

You can read more about the impact of this in the GB Outlook here.

When compiling a custom run for a site over 300MW, we use a method which depends on the revenue stream. This applies from v3.3 of the forecast.

Frequency response revenues

- We anticipate that for a large site, the majority of the business case will be in merchant markets. However, it is reasonable to expect that some part of a large site will participate in ancillary services. So, we take frequency response as the first 100MW of the site from our ancillary-focus Central scenario.

Day-ahead and intraday revenues :

- We model the growth of GB-wide battery capacity in our battery buildout projections, which include capacity from large sites. We also model the impact of this growing fleet of battery storage on suppressing price spreads in both Day-ahead and intraday price forecasts. The fleet of batteries acts to smooth price spikes (and troughs), and not all assets get the 'most' optimal price.

- However, in the dispatch model, we model each site to dispatch optimally against the given price signal: the individual site sees - and 'gets' - the best available price. For a large site, which is probably going to be split into multiple units and operated by one party, this could present an issue. Volume should not be put into the same market at the same time, as an excess of volume will likely cause the forecast high price to fall in that market. This is particularly in continuous intraday markets where the median volume traded in any one settlement period is around 3GWh.

- To caveat this, the intraday prices themselves already capture the impact of multiple GW of battery capacity reducing price volatility. If we added an additional suppression due to liquidity considerations on a large battery site (with multiple units), we would be double-counting the effect.

- So, intraday and day-ahead revenues remain the same as in our Central scenario, and we take 100MW from ancillary-focussed and the rest from the merchant-focussed strategy.

Balancing Mechanism revenues

- Balancing Mechanism actions can be split into energy and system actions, and some of these actions have a natural depth of the market, which a big BESS site is likely to saturate. There is a locational element to system actions: the NESO control room will only want a limited amount of bid or offer volume behind (or in front of) a constraint to resolve whatever issue they are solving. There is also a limited volume that the control room will take to correct grid frequency (batteries are often used for frequency control via the Balancing Mechanism due to their fast response speeds). Too much, and grid frequency is likely to bounce in the other direction. This limited depth will impact Balancing Mechanism revenues at large battery sites.

- To account for this, we put a haircut on BM revenues relative to our Central case. The haircut depends on the site size (which is behind the same Grid Supply Point), with larger sites seeing a bigger haircut.

- Some projected large battery sites are approaching the size of CCGTs. So, to examine the possible impact of site size on BM revenues, we use BM data from the gas fleet and find that larger assets, proportionally, have less volume dispatched. Volume translates into revenues, so fitting the data, we get to a haircut on BM revenues taken from our Central Scenario for all sites over 300MW.

Updated 9 months ago