Large >300MW BESS sites (v32)

We do not recommend using our Central curve to forecast (very) large BESS sites.

A battery of 50MW is a different proposition to one of 1000MW, so we have an alternate way of producing curves for these assets.

Essentially, we expect a lower £/MW/year.

You can access a forecast for a large asset via a single custom run, submitting the details of the single large site which we will break down as detailed below.

If you intend on breaking the large asset into several BMUs but these will all sit at the same Grid Supply Point, please submit the whole site to avoid inaccurate revenue curves.

What does large mean?

There is a ramp rate restriction on any single generator site at a Grid Supply Point that kicks in at 300MW. For this reason, we determine that 'large' is anything over 300 MW (BC.1.A.1.1. of the Balancing Code, here).

How many 'large' sites are operational now?

Currently, there are 4 BESS sites operational with a size of 100MW each:

- Dollymans, which exists as a single BM unit of 100MW (100MWh)

- Minety, which is split into Minety Lower and Minety Upper, both 50MW (56MWh)

- Capenhurst, which is split into 4 x 25MW (26MWh) units

- In October 2024, Lakeside became operational, 100MW (200MWh).

There is another asset due to come on soon, Blackhillock, which is 200MW (400MWh), and will be split into two BM units. Stratera's Thurrock (300MW, 600MWh) is also due online soon.

However, in 2025 and 2026, we expect more larger assets to come online, and the Modo buildout report includes a number of projects >300MW.

How might a site > 300MW be operated?

It's difficult to say exactly, as we don't have any operational right now!

Big BESS sites are likely to be split into several sub-units – a 1GW BESS might (for example) be split into 6, and (some of their) operations may resemble pumped hydro - more like Dinorwig!

- One (or more) subunits might be contracted under longer-term contracts or tolled, hedging some of the risk and probably taking a lower £/MW as a result.

- Other units will be exposed to merchant revenues. These revenues are lower purely due to the ramp rates restrictions on such a unit as per the Balancing & Settlement Code (BC.1.A.1.1.)

- Parts of one of the units might hold an ancillary service contract. There is (October 2024) a limit on the amount of frequency response a single unit can delivery: 50MW for DR and DM, and 100MW for DC. We expect all three to be at a 100MW limit by the end of the year. Of course, these markets are already fully saturated - we would not forecast any sub-unit to be delivering these services at its full capacity.

- For usage in the Balancing Mechanism, dispatch rates are likely to be much higher, but the amount of energy used is not likely to be the full capacity of the system, as the control room won’t always need 500MW+.

Our central forecast won’t capture all of these nuances.

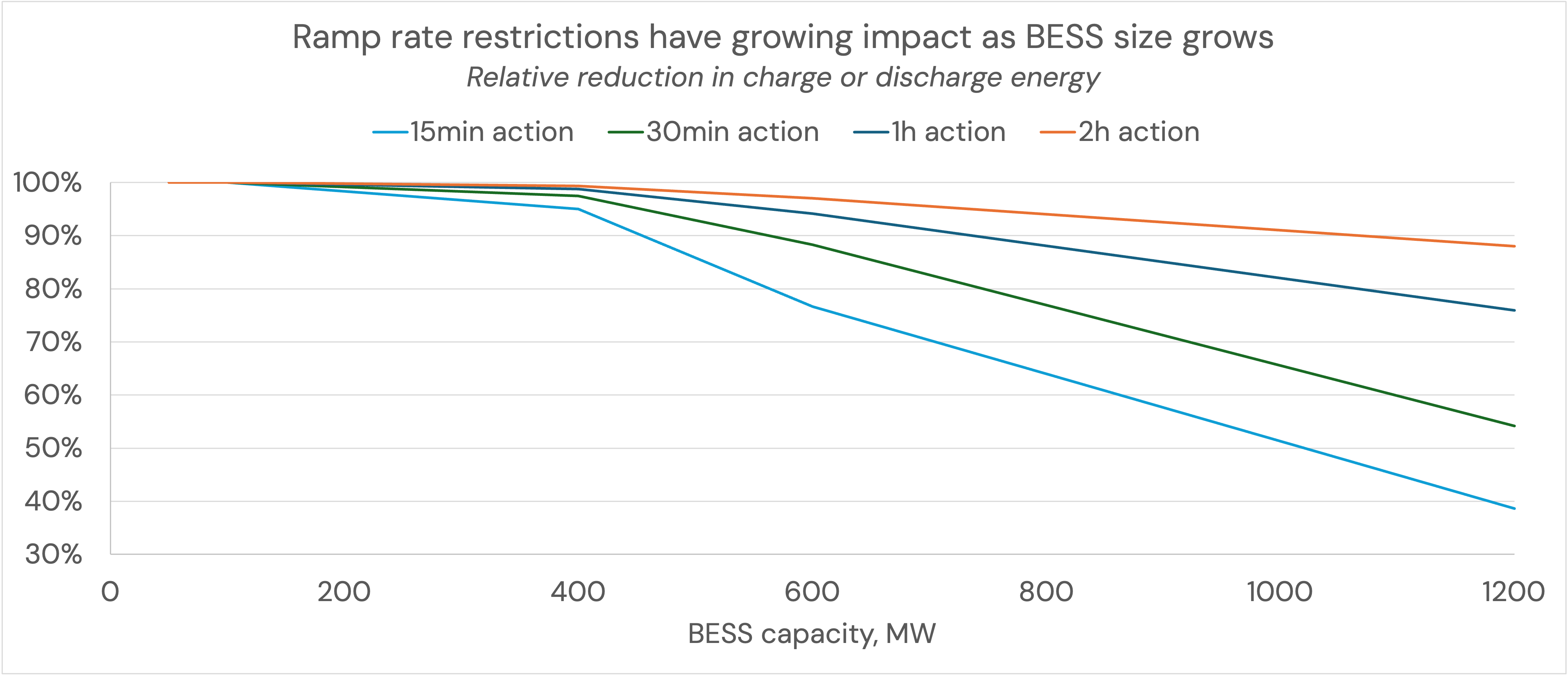

What impact do these ramp rate restrictions have?

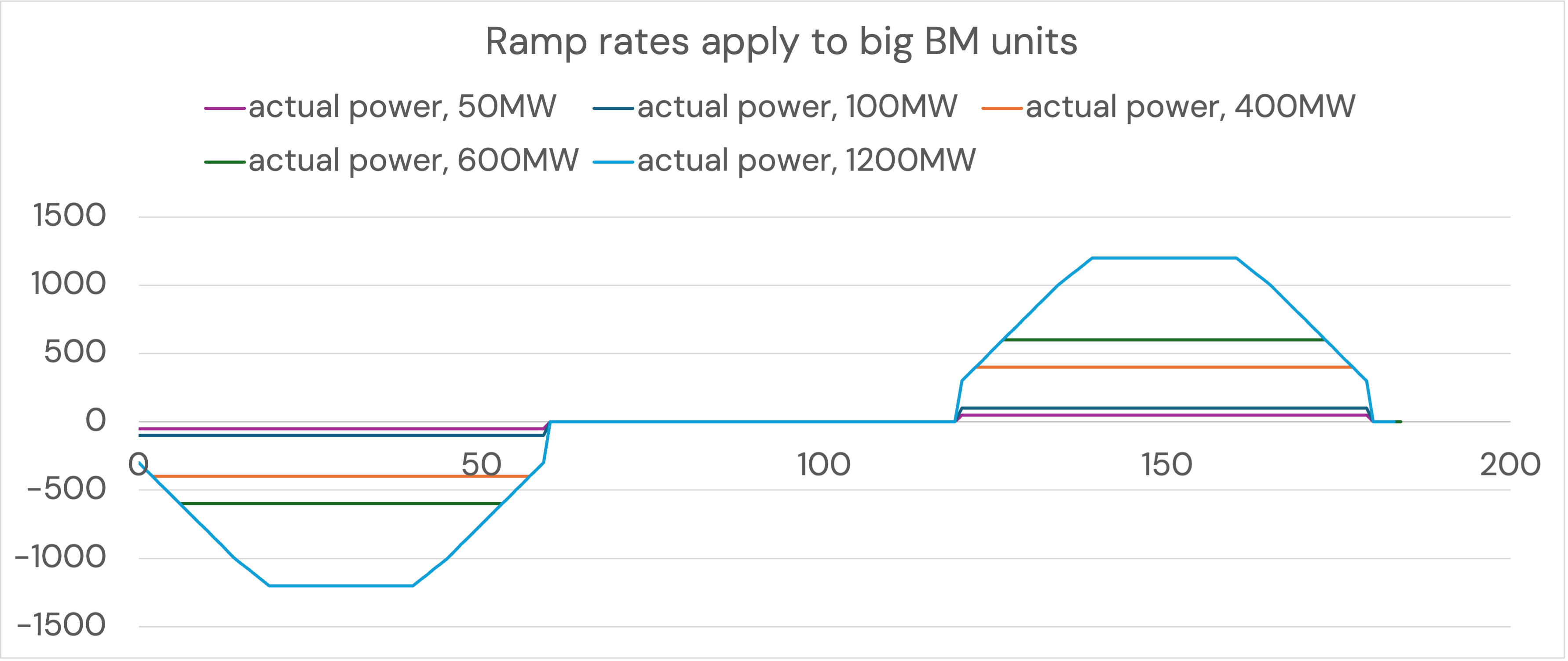

The amount of energy that can be charged and discharged is restricted, depending on the duration of the action. An example of a 1 hour charge and discharge is shown below, for different sized BM units. The longer the duration of charge or discharge, the lower the impact.

These ramp rates do not apply in the Balancing Mechanism.

Modeling the revenue stack of assets > 300MW

In v3.2 of the Modo forecast, we have modified the dispatch model to account for the ramp rate restrictions shown above. We also cap any ancillary service contact to 100MW.

You can read more about the impact of this in the GB Outlook, here.

When compiling a custom run for a site over 300MW, we follow the method below, which blends our low and central scenarios. On a £/MW basis, a large site will earn less.

- First 100MW

100MW of ancillary-focused strategy (central scenario): driven by the cap on unit size in dynamic frequency response services. There will be day ahead, intraday revenues, balancing mechanism, as well as frequency response revenues here.

- Next 200MW (total 300MW)

200MW of merchant-focused strategy (central scenario)

- Next 300MW (total 600MW)

300MW of merchant-focused strategy (low scenario).

The second portion is likely to return a lower £/MW than the first 300MW, in a similar way to the second hour of wholesale trading is worth less than the first.

We recommend using our low scenario for this portion of the site's revenues. This portion will be merchant only, but restricted by ramp rates.

- Next 300MW (total 900MW)

300MW of merchant-focused strategy (low scenario).

These rules apply even if the you are looking at a portion of a larger site, say 250MW of a 1GW site.

Updated 2 months ago