Storage (v3.4)

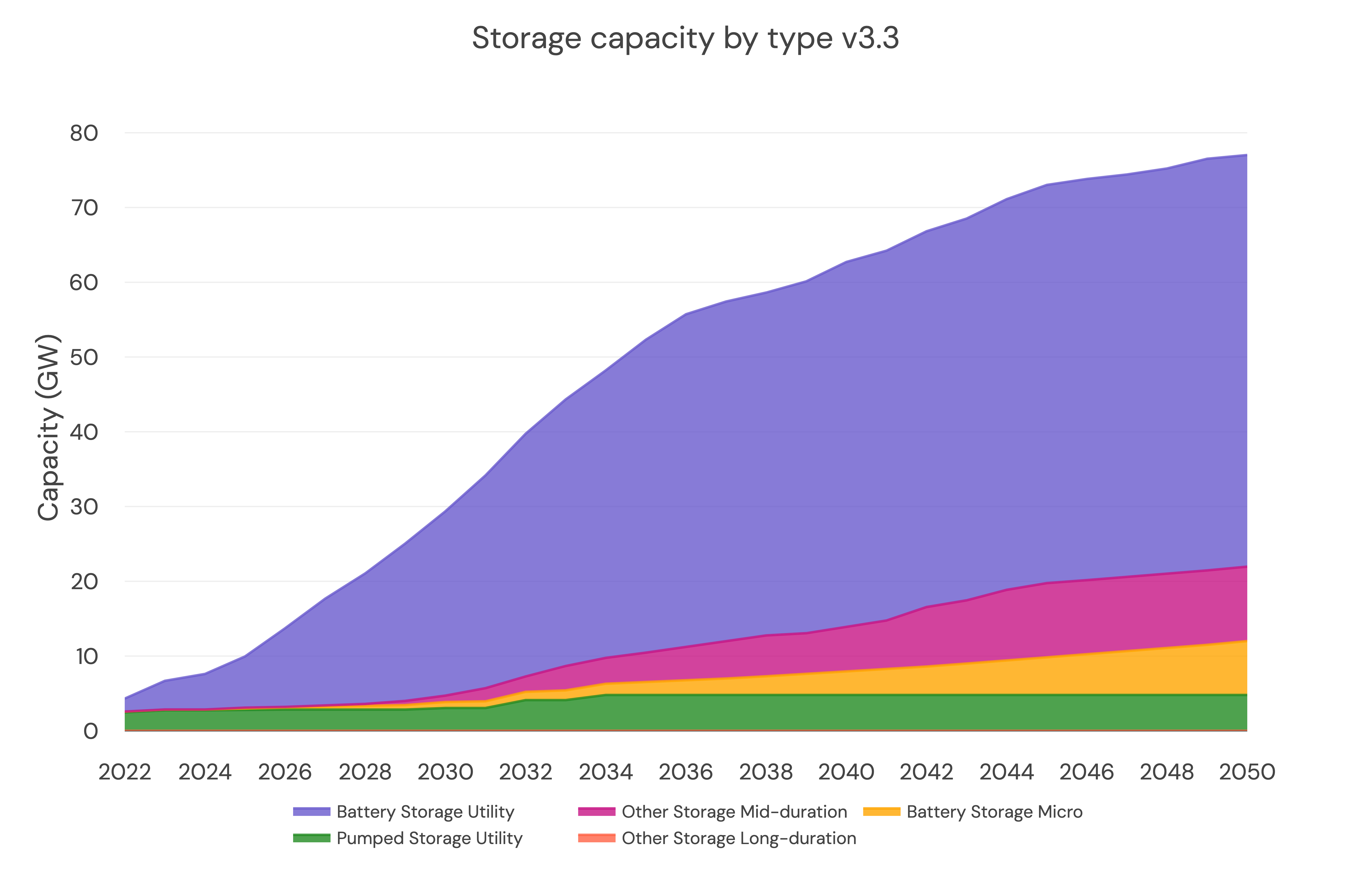

There is 80GW of energy storage on the system by 2050

The FES Consumer Transformation scenario (2023) put 35GW of storage on the system by 2050, but we think that's not enough.

And our capacity expansion model agrees!

The 2023 CM auctions (a good way of assessing how many projects are at a stage where the developers are confident they'll get built as non-delivery penalties are high) show 12GW of battery storage by 2027.

The Q2 2024 buildout report shows 14 GW by the end of 2027.

Let's consider the global growth of energy storage, as put by Michael Liebreich:

The same thing has been happening for batteries – they have in fact been racing through doublings even faster than solar: five of them in the last eight years. In 2015, some 36GWh of lithium-ion batteries were produced; last year the total was around 1TWh. Over the past decade, cell costs have come down from $1,000 to $72 per kWh, and at the same time energy density has doubled and degradation per cycle has halved. We are also seeing new battery chemistries such as iron-air and sodium-ion that promise to be even cheaper than lithium-ion.

Battery energy storage is the only non-subsidized, commercially proven, scaled technology that can manage renewable intermittency, grid constraints, balancing, etc.

CATL has recently released new numbers for their battery cells, reducing cell costs by $100/kW.

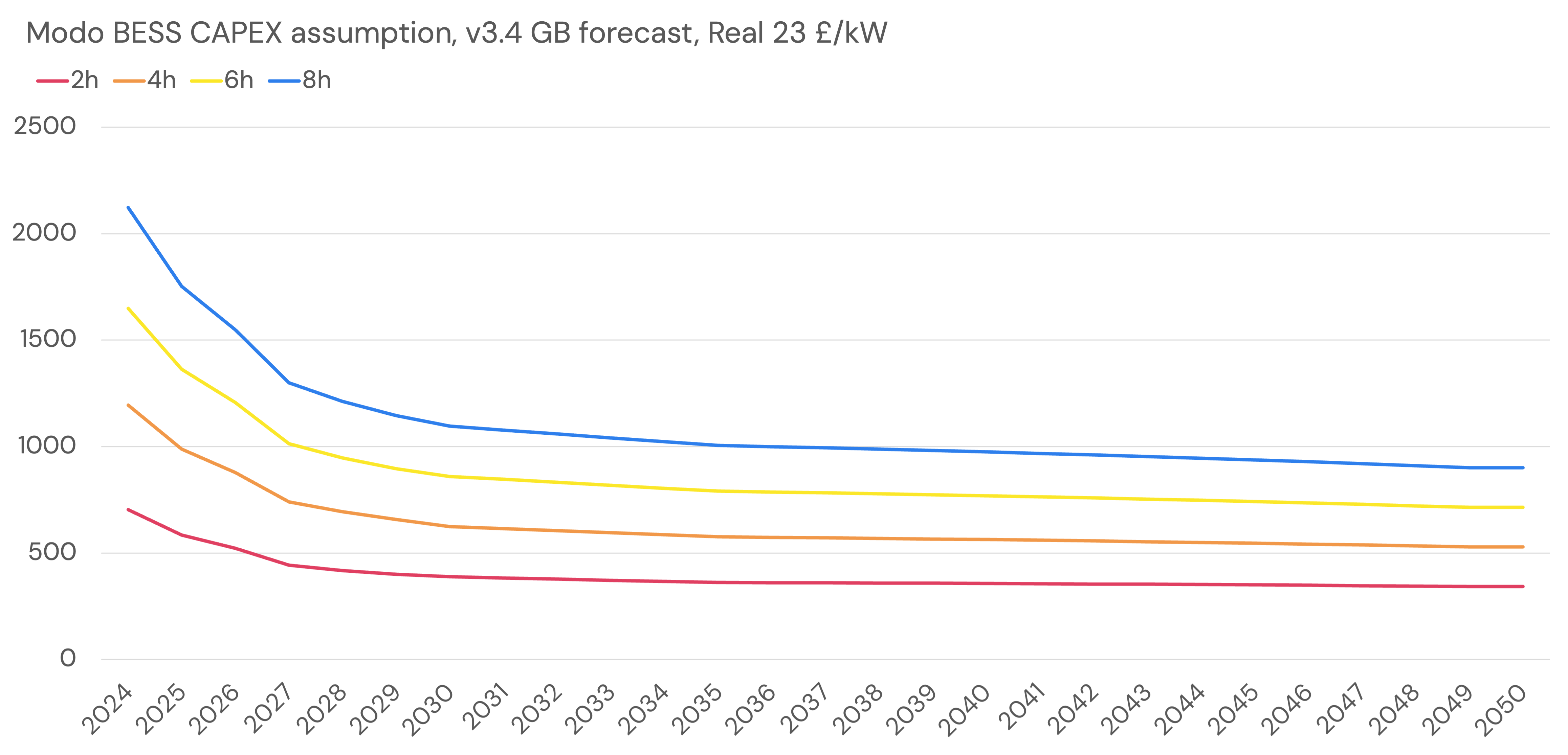

Battery CAPEX has dropped in the last year and will continue to fall

Major battery manufacturers (CATL, for example) announced dramatic drops in the cost of their systems in the first half of 2024. In November 2024, Modo conducted a survey covering 2.8 GW of battery energy storage projects - with commissioning dates from 2024 to 2028. 30 responses detailed costs from the GB storage industry on the CAPEX of their previous or next project. Costs are adjusted to Real 2023 values.

These are blended with CAPEX figures from National Renewable Energy Laboratory (NREL, 2023) adjusted to Real 2023, where learning rates for CAPEX costs to 2050 and CAPEX for ratios between 2, 4 and 6 hour systems are incorporated.

CAPEX includes cost of grid connection, Balance of Plant and Containerized cell costs. It can be read as an 'all-in' figure.

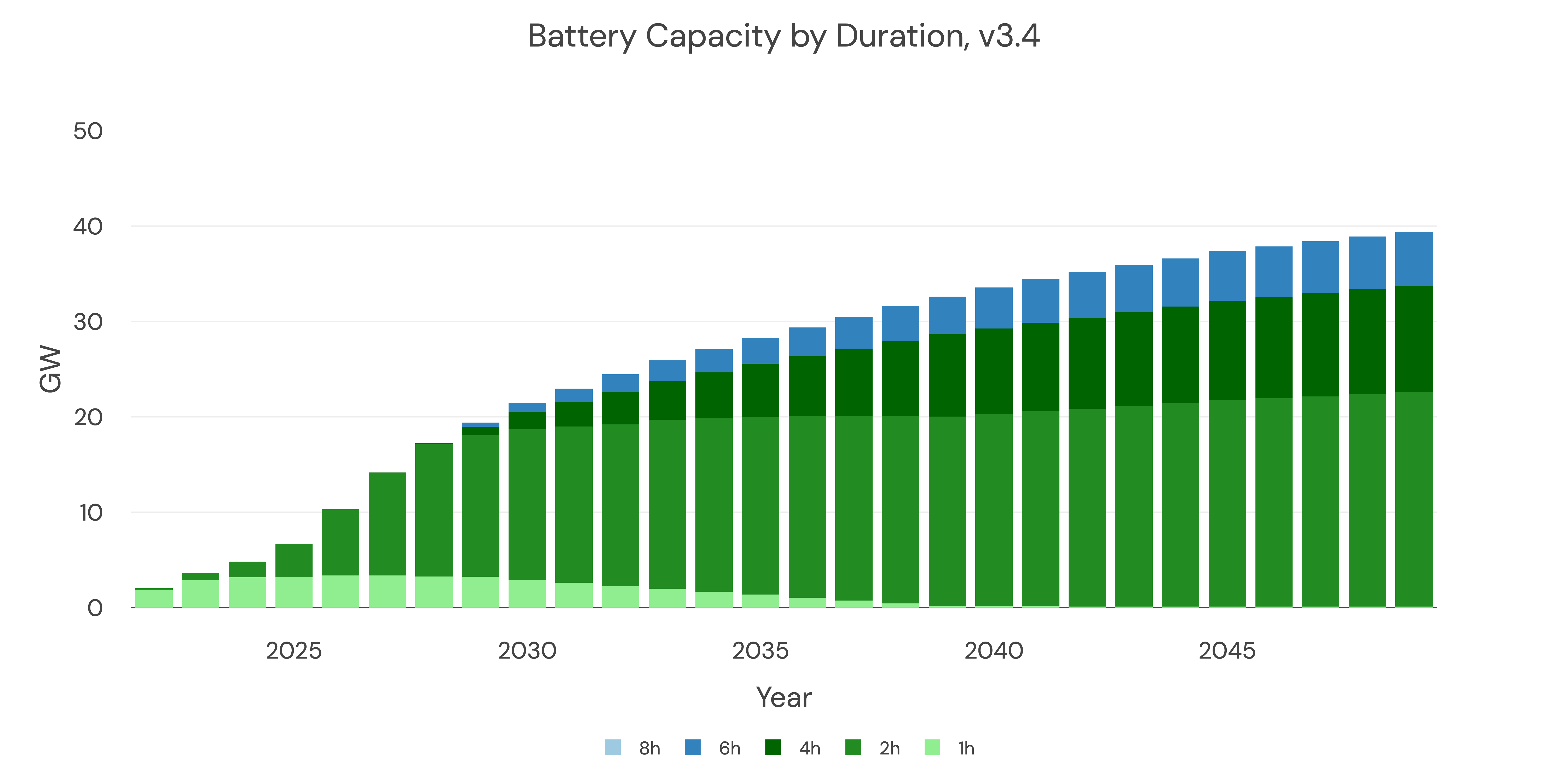

Utility-scale battery buildout

Our capacity expansion model is informed by the learning rate of battery CAPEX (as per the figures above). We model the Capacity Market and wholesale revenues for trading storage to determine their profitability for 2, 4, 6, and 8-hour systems.

Modo Energy anticipates a slower build-out of battery storage by 2030 than the national targets in Clean Power 2030 (CP30).

There is uncertainty in the GB BESS market due to policy changes as a result of REMA, Connections Reform, the Strategic Spatial Energy Plan and Clean Power 2030. This has slowed investment decisions, which will slow future operational dates of new sites. In addition, we have never built as much storage as the CP30 targets suggest will be built in the next five years.

Post-2030, centralised targets for battery buildout are under review, and initially look flat. Questions remain over even getting a grid connection for a new storage site to come online after 2030.

Modo Energy's position is that while the industry will miss the CP30 storage targets by 2030, we will hit them by 2035. Post-2035, with continuing falls in battery CAPEX and a growing requirement for balancing from a growing renewable buildout, we anticipate more battery storage to come online. We model 6h systems to pass a 10% IRR threshold from 2030 onwards.

We assume no new 1-hour systems get built, and the existing 1-hour fleet get augmented to 4-hour systems from 2030 onwards.

The duration of storage in the buildout is shown below.

Considering also behind-the-meter battery storage, and other types of storage, the build-out is:

Values for pumped and other storage are taken from the 2023 FES.

Pumped storage capacity will also grow

The FES says that an additional 3GW of pumped storage will come online in the early 2030s. This is largely driven by a significant new project (Coire Glas) in Scotland and the conversion of smaller hydro sites to pumped hydro.

Other storage will come online

Likely to be from liquid and compressed air storage, we also have mid-duration storage coming online.

Updated 7 months ago