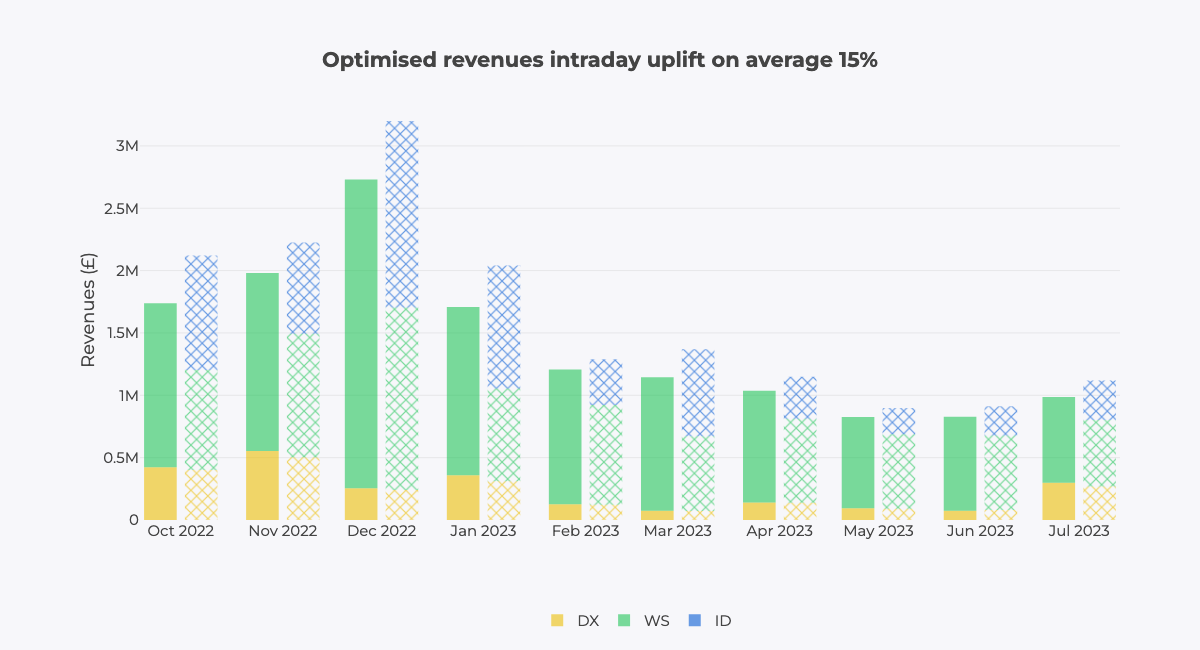

Intraday revenues

How we model the uplift of day ahead and intraday trading

Rather than modeling future intraday prices and optimising against them. We model the intraday revenue uplift. That is, the revenue uplift due to optimizing in day-ahead wholesale, frequency response and intraday, compared with optimizing in only day-ahead wholesale and frequency response.

In other words, how much can day-ahead revenues be improved by allowing optimization in the intraday market.

How do we optimize for intraday prices to quantify uplift?

We calculate historical intraday revenues using the dispatch model with and without intraday prices. This is the RIPD of the EPEX intraday orders. As a result, the most optimal charge and discharge schedule changes, and the revenues shift.

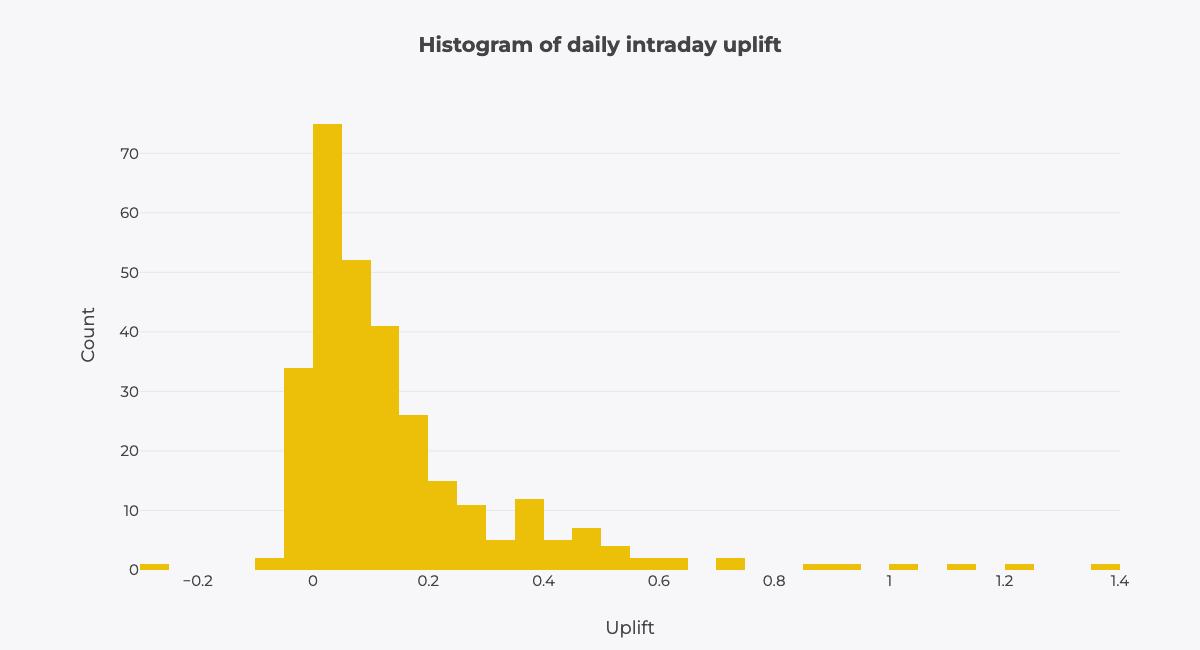

On average the daily revenue uplift due to including intraday prices is 15%. The median uplift is slightly lower at 9%. This is because mean uplift is increased by extreme days with very high intraday revenues.

We know this is a very simplified approach...

We also looked at the relationship between intraday prices and potential drivers, including: wind generation, margin, demand and wholesale prices. There were no clear correlations and intraday price prediction methods performed poorly when backtested.

So, we assume, going forward, a similar situation to today; in that the intraday uplift is 15% of the DA value - mindful that this is probably quite conservative given the large tail in the distribution above.

Updated 5 months ago