Inputs: capacity stack

What goes into the generation mix?

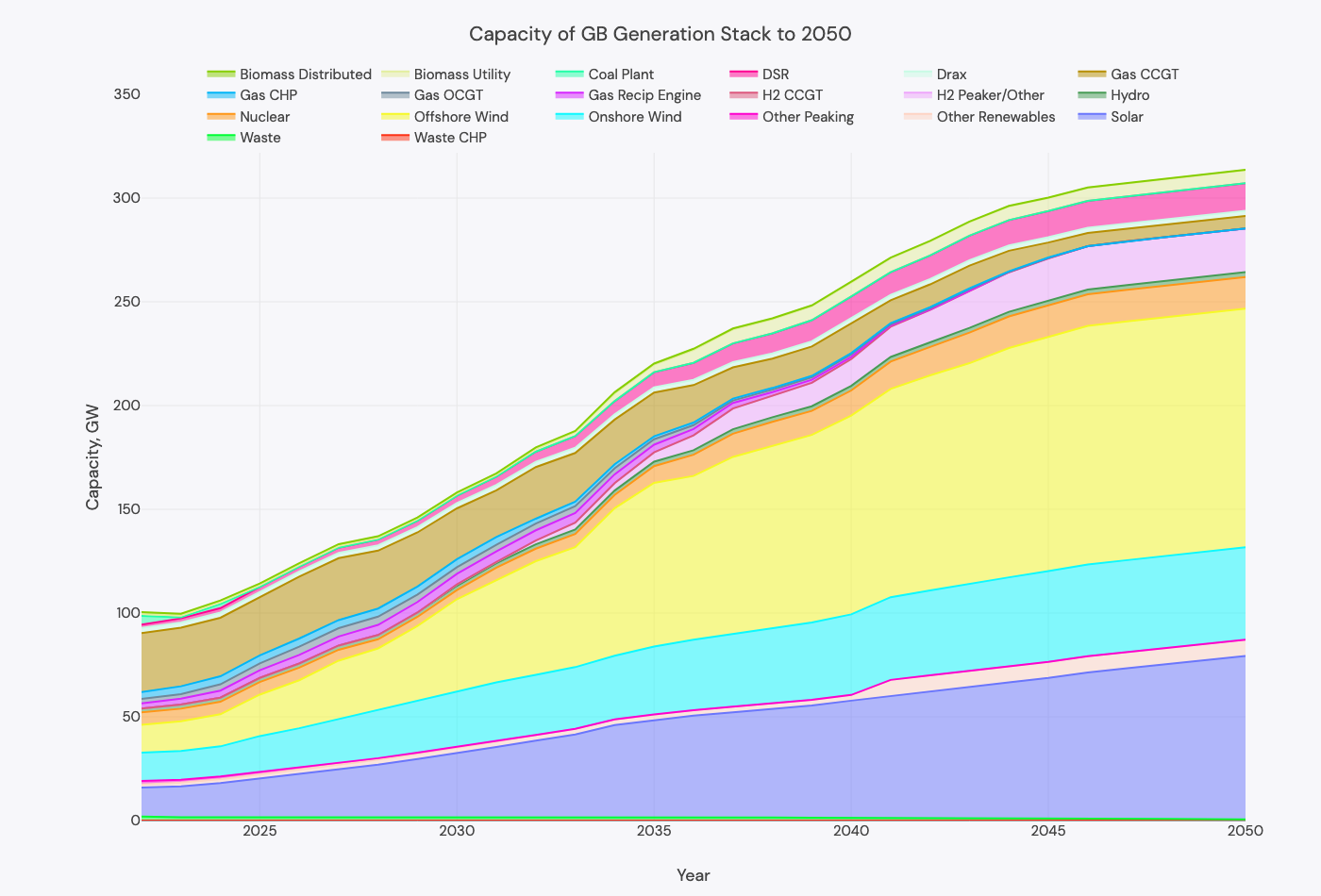

GB will have over 300GW of connected generation by 2050

Here's the full capacity stack from 2023 - 2050. We'll break this down bit by bit below.

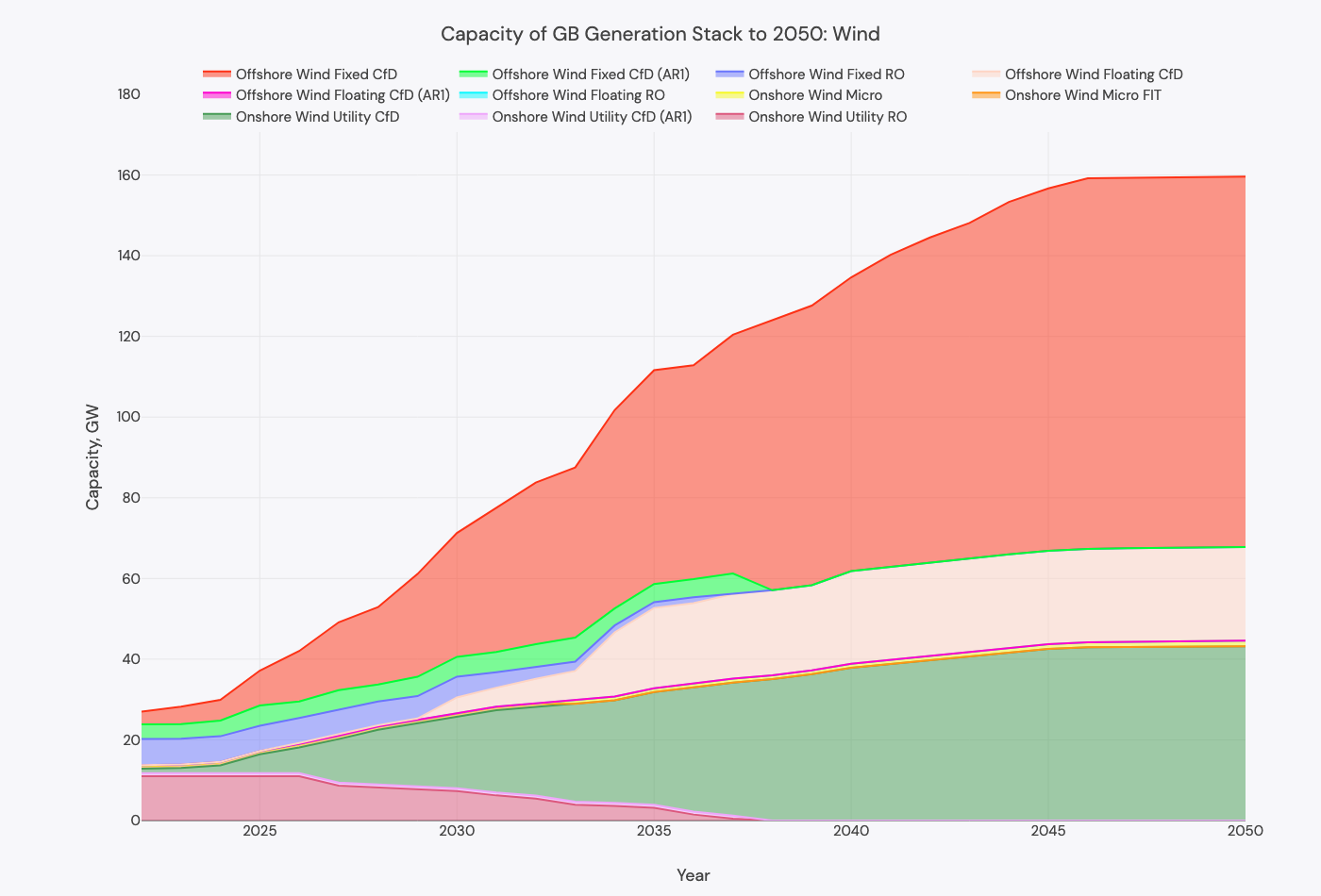

Wind Capacity at 150 GW by 2050 with over 100 GW of it offshore

From now until 2035, we get individual offshore wind farm capacity from our build-out pipeline. We know what has a Contract for Difference (CfD) contract and what gets Renewable Obligation certificates, so we can work out what is subsidized. The recent AR5 has not yet been accounted for but we are working on updating the model to reflect this very soon.

Similarly, until 2035 we get individual onshore wind farm capacity from Renewable Obligation and Feed in Tariff registers. We remove these from the pre-2035 FES numbers for onshore wind and get a subsidized and unsubsidized pipeline.

We assume all new CfDs going forward are floored at £0/MWh, and early rounds (labelled AR1 in the figure) are priced at £100/MWh. Onshore wind and solar PV were not eligible for CfDs in AR2 or AR3.

After 2035, we take buildout numbers from the FES.

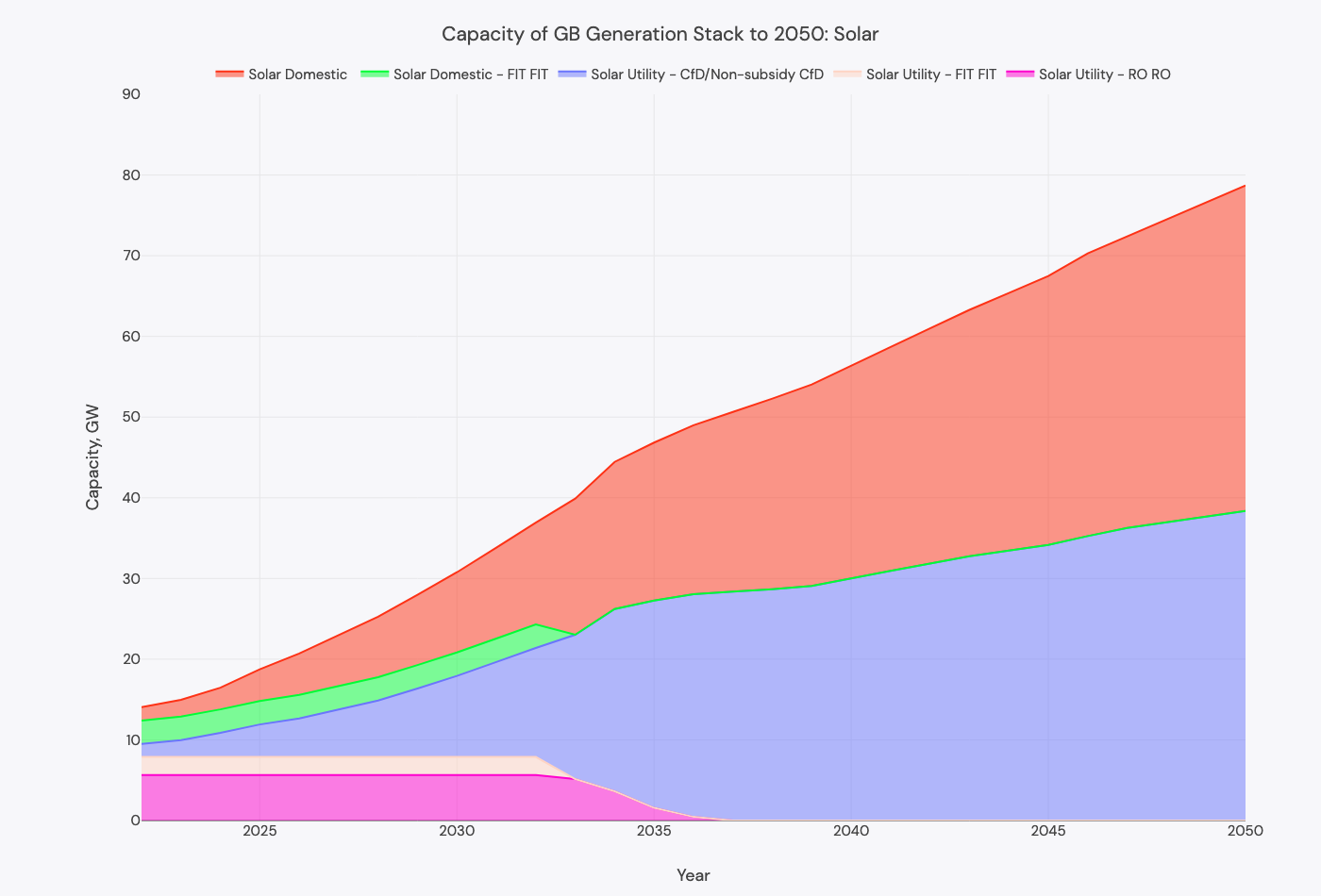

Subsidized solar retires whilst domestic and unsubsidized utility PV gets to 80GW by 2050

For solar, from now until 2035, we use the Renewable Obligation and Feed-in-Tariff registers. We extract these numbers from those in the FES to get an unsubsidized and subsidized pipeline to 2050.

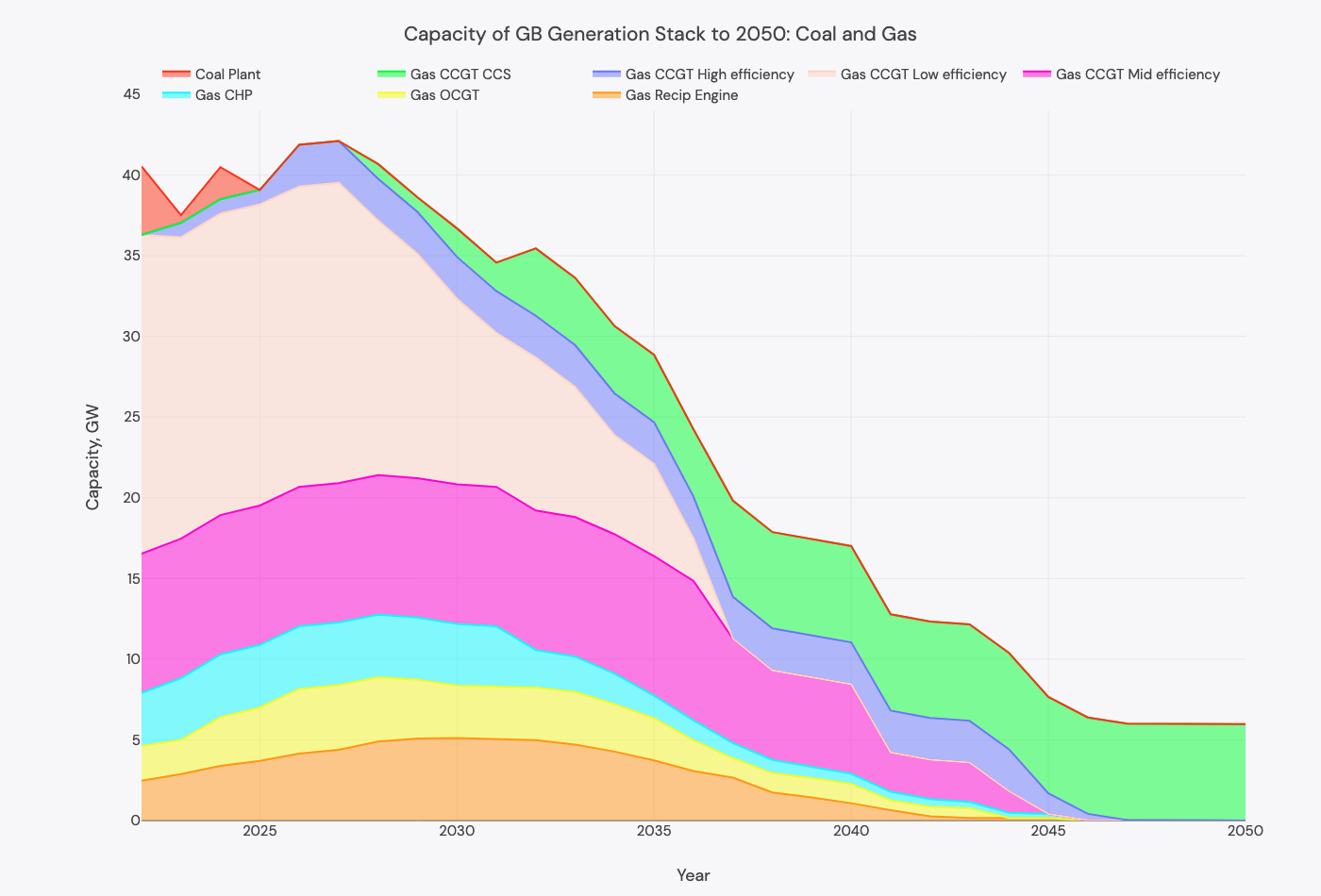

Gas: low-efficiency CCGT goes by 2038, with CCS picking up after 2030

Until 2035, we model each individual CCGT from our build-out pipeline.

These are grouped by age to retirement and efficiency: older assets are the least efficient and retire first.

After 2035, we take the numbers from the FES, but prolong the life of some units in response to high loss of load on the system in their absence (and increase Capacity Market clearing prices to let this happen).

Gas CHPs are assumed to be largely non-dispatchable and sit embedded in the distribution network. OCGTs fall out of the stack by 2045, and gas reciprocating engines grow in capacity in the early 2030s before coming offline in the early 2040s. These numbers are all taken from the FES.

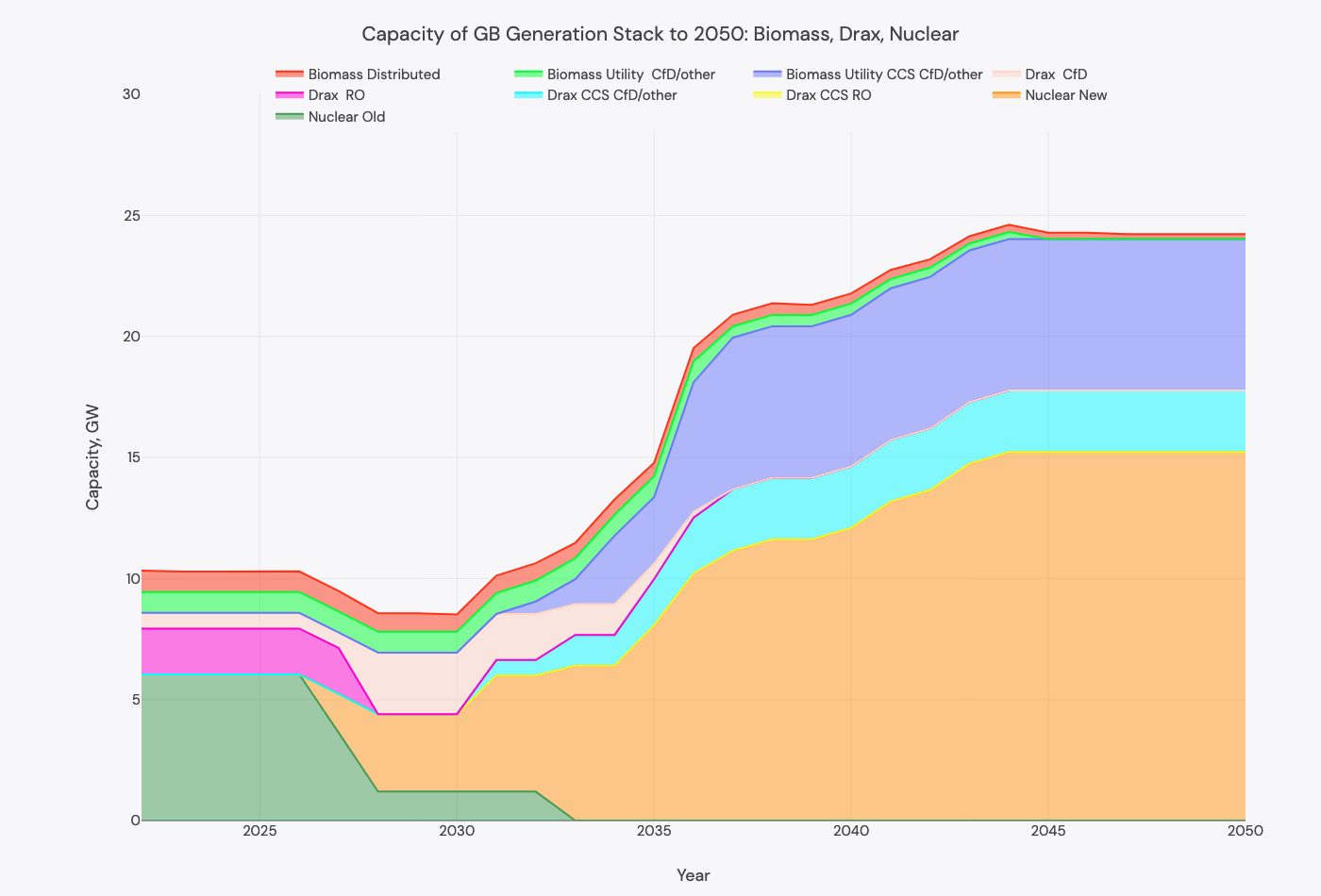

Low carbon baseload provided by biomass and new nuclear

We take biomass numbers from the FES, and separate out Drax from this capacity as their public accounts give extra information (particularly around CCS).

Old nuclear consists of Hartlepool, Heysham 1 and 2, Torness, and Sizewell B. New nuclear consists of Hinkley Point C (online in 2027 and 2028), Sizewell C (in 2031 and 2033), along with 8.8GW of other new nuclear from 2035.

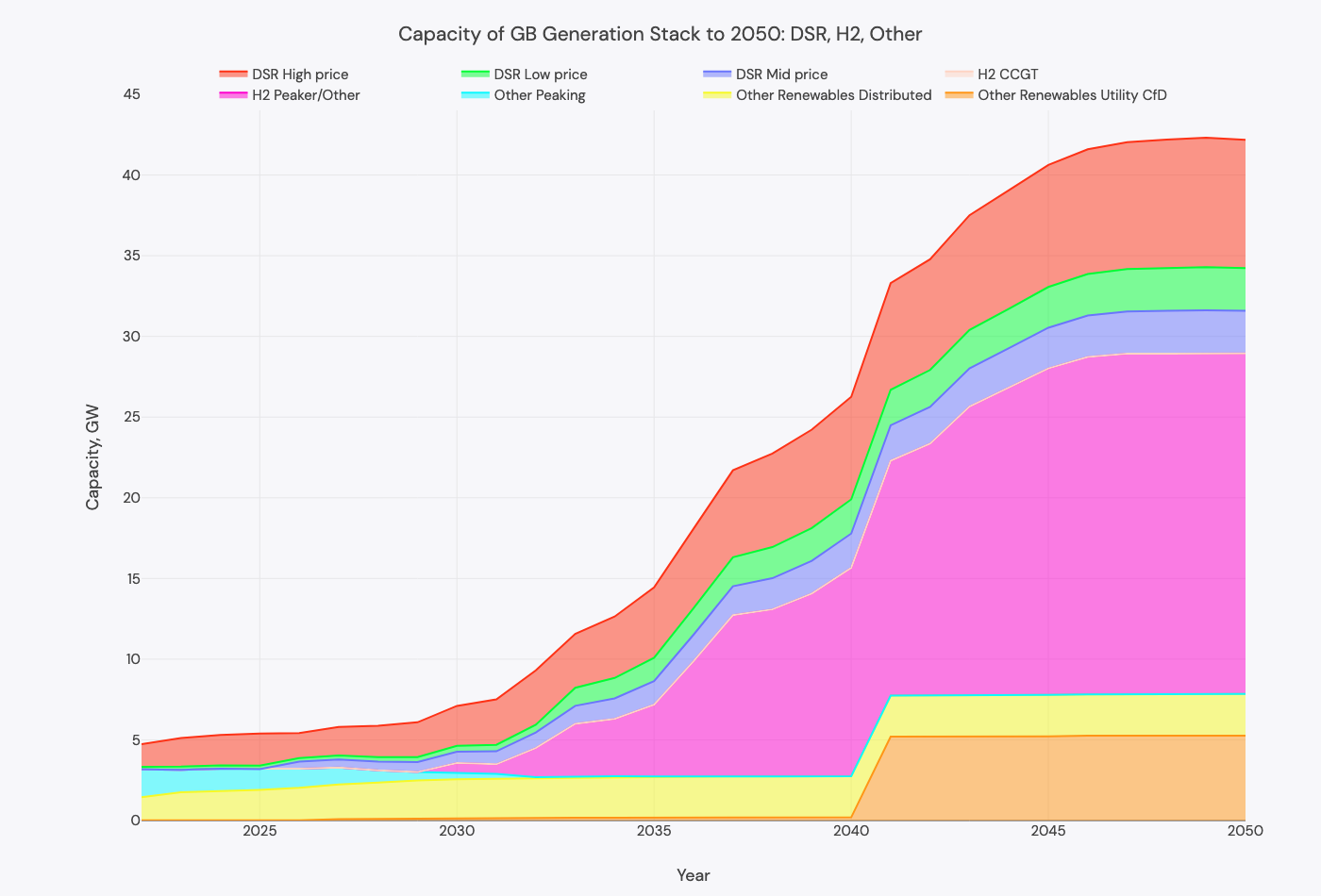

Other peaking technologies from DSR and hydrogen

The FES provides a guide on hydrogen capacity but doesn't dictate what it is. We assume it's all peaking as we don't think a hydrogen CCGT makes economic sense. More on that next.

Demand Side Response (DSR) is given three subtypes: Low, Mid and High price. This indicates the cost of using it (i.e. how easily it can be used) at times of system stress. Low is priced at £500/MWh, Mid at £1000/MWh, and High at £3000/MWh.

Updated 5 months ago