v3.4 release: changes since v3.3

8th April 2025

Hope you've been enjoying the sunny spring days of late!

The changes to the GB forecast over the last 3 months include new gas prices, updated battery CAPEX, a lower BESS buildout due to changes in the market due to connections reform, and longer duration storage coming online. We've also improved our Balancing Mechanism model.

Updated commodity prices

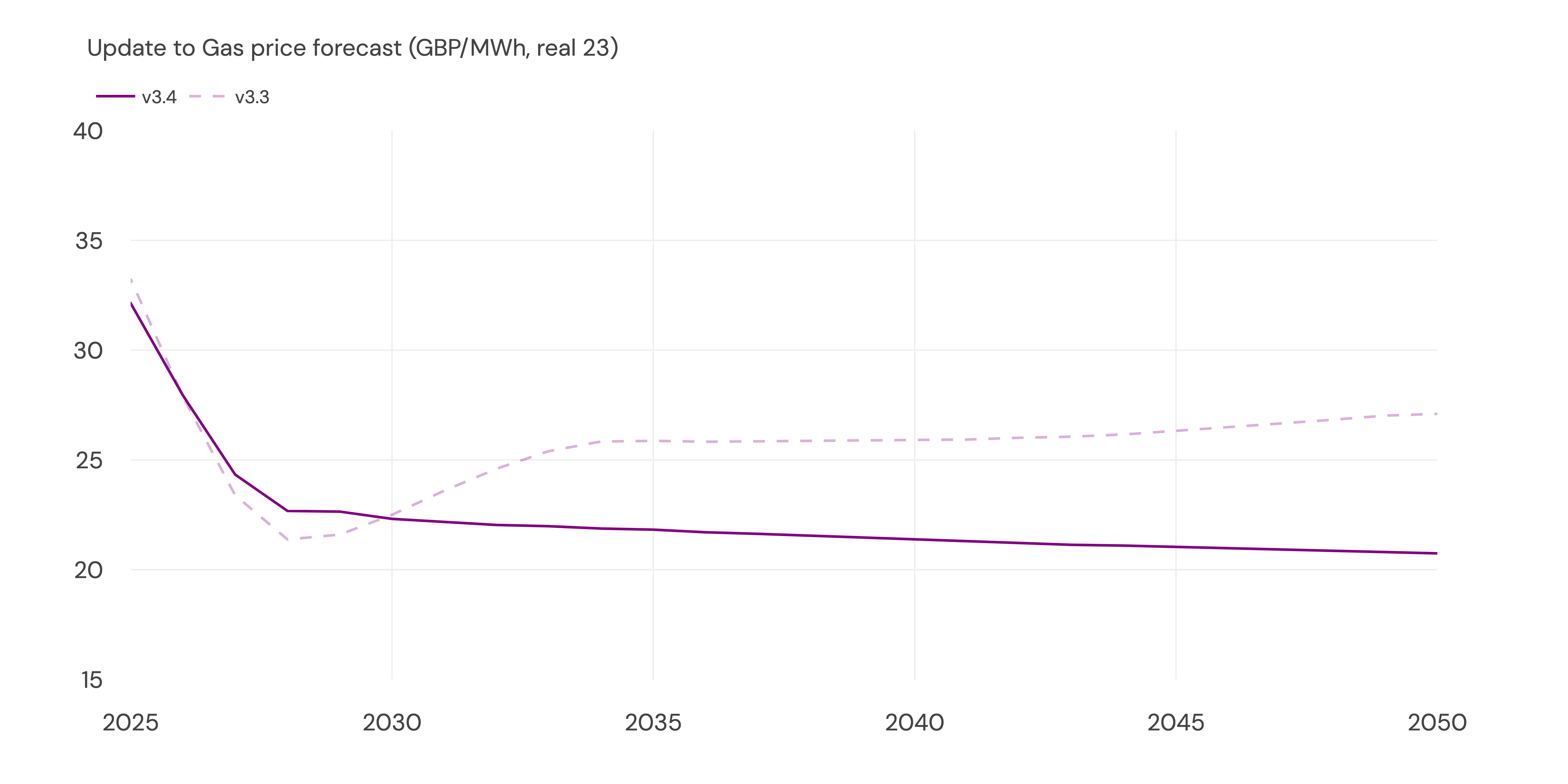

Gas price

Previously, we used gas price inputs from CME's forward curve with the longer-term forecast from NESO's Future Energy Scenarios.

After reviewing a range of data sources for long-term gas price forecasts, we have chosen to create a blend of Oxford Economics, Deloitte, and CME's forward curve.

The comparison of these is below.

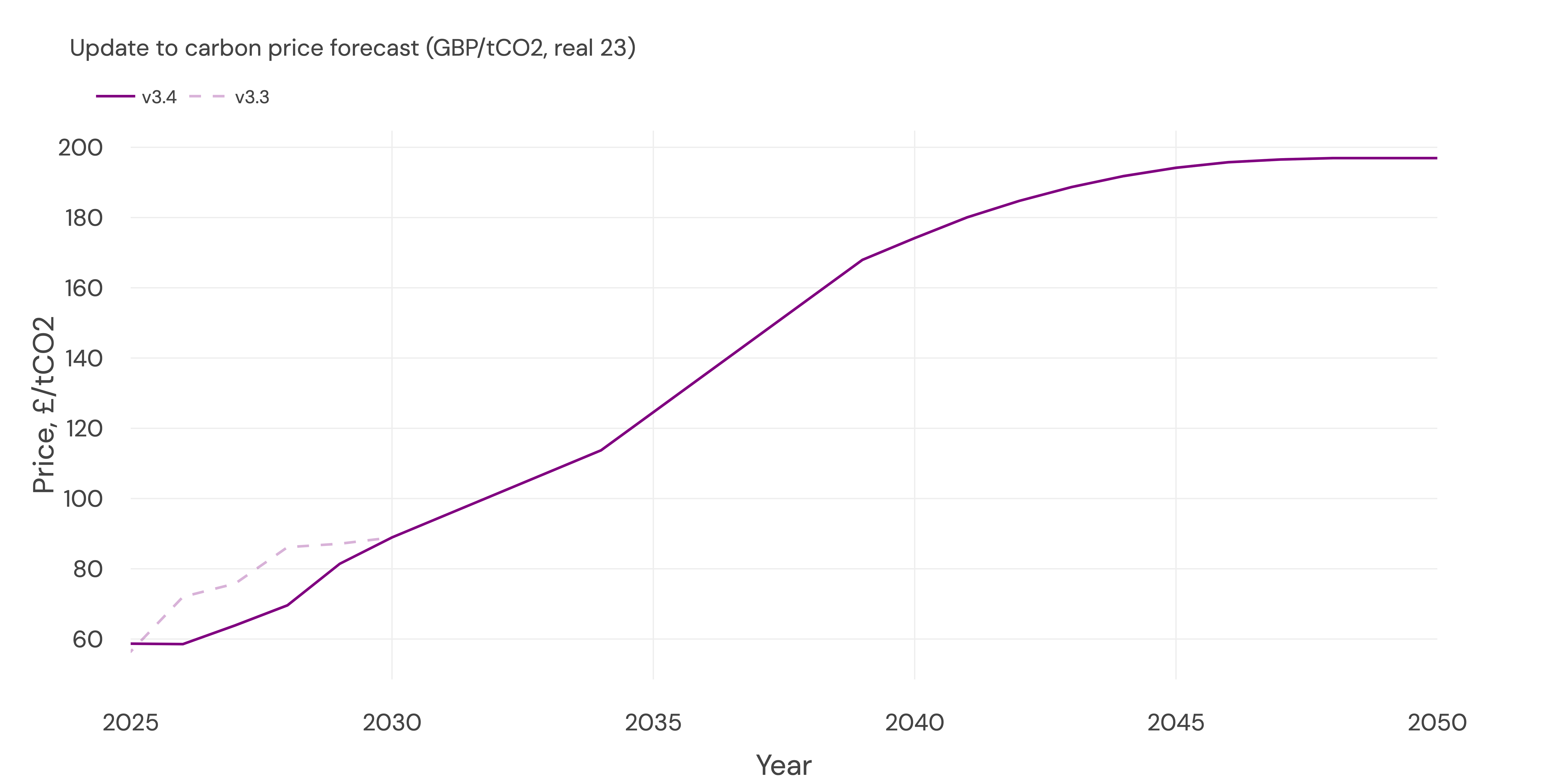

Carbon price

These are higher in the short term due to changes in the forward curves, leading to higher spreads.

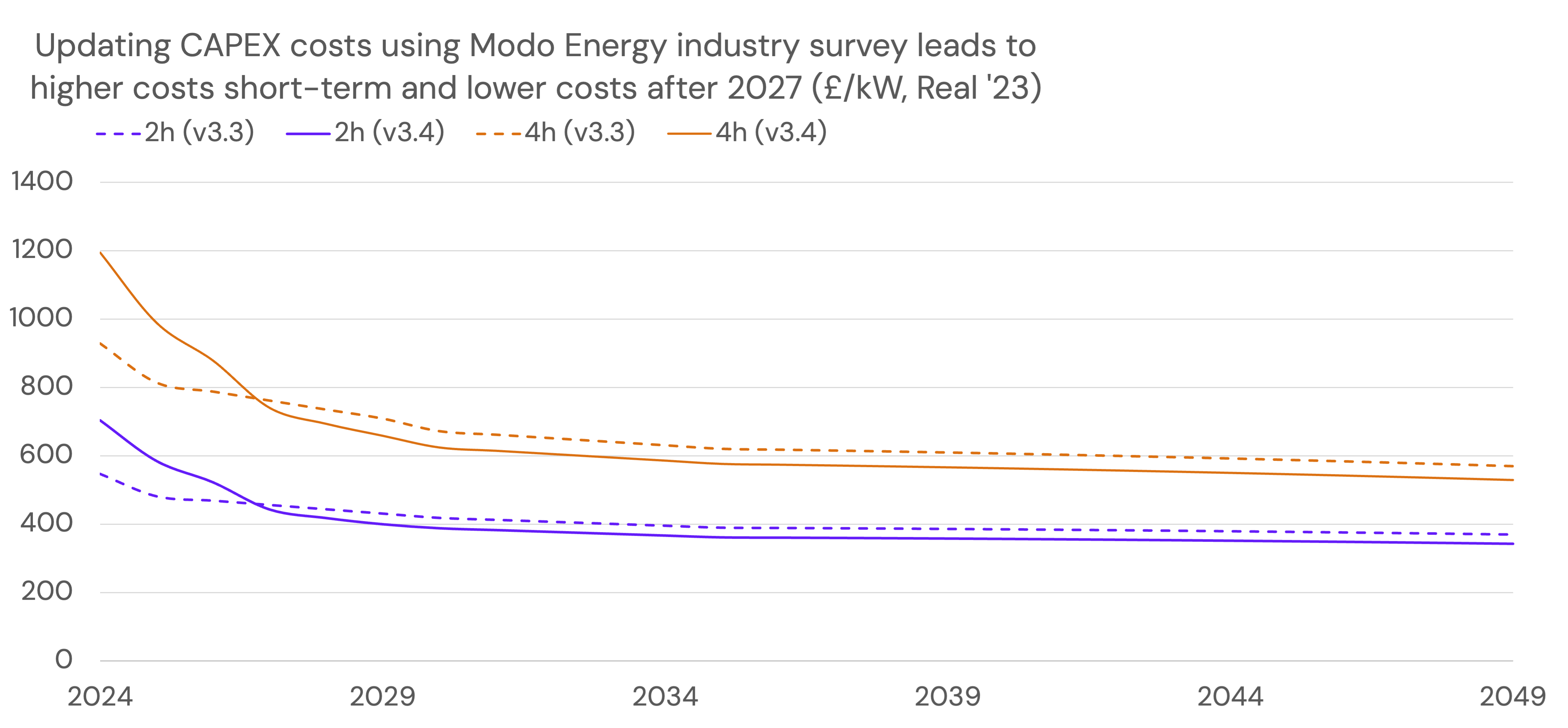

Updated BESS capex

In line with results from Modo's recent CAPEX survey, we have updated our assumptions on battery costs.

Costs are slightly higher than previously assumed to 2026, and then drop to a slightly lower value long term.

More information is here.

The effect is that we now reach higher IRR values for longer-duration systems and, as a result, build more longer-duration battery systems within our capacity expansion model.

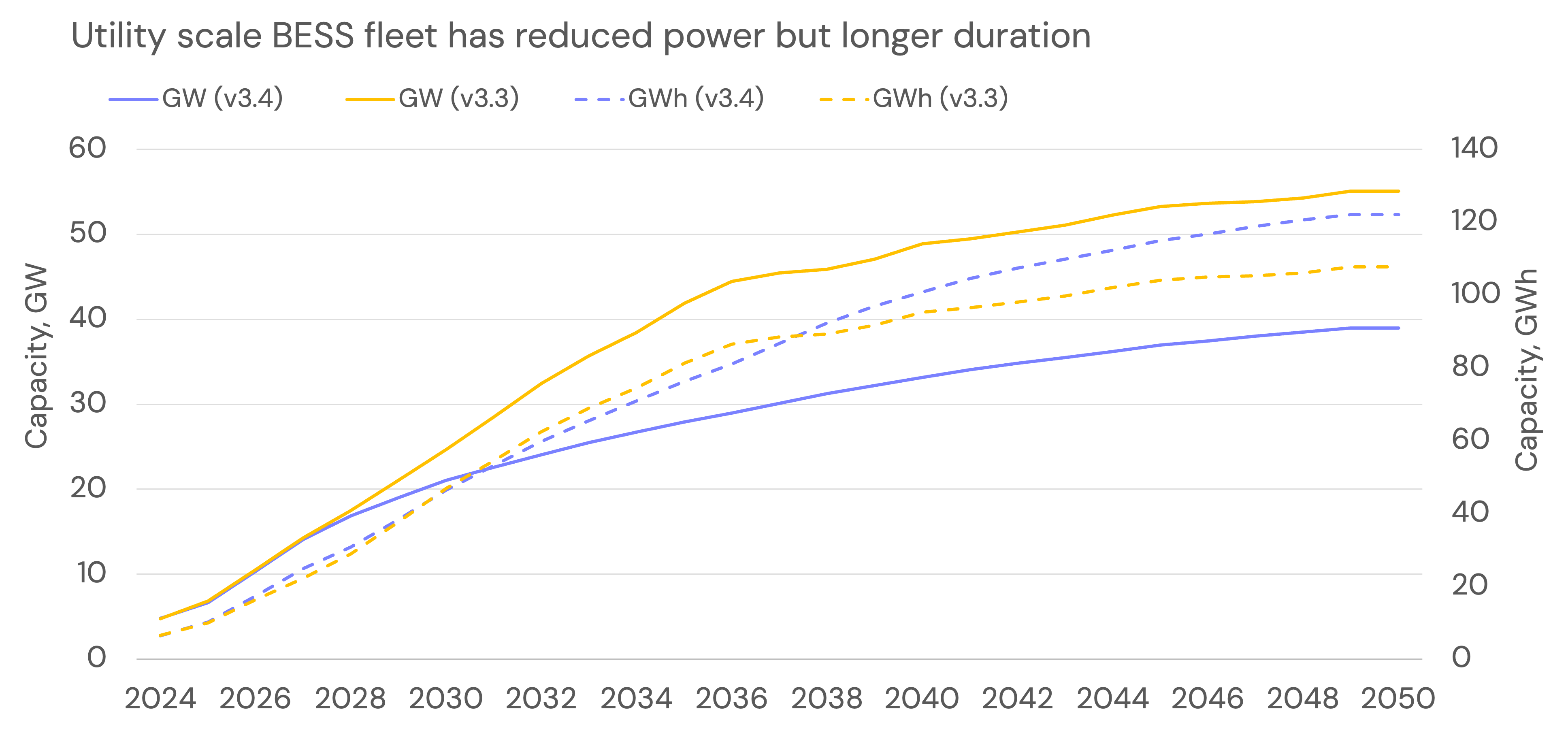

Impact of connections reform and policy changes causing uncertainty in the market on the BESS buildout

We have updated the early years of our battery buildout using the latest Modo buildout report. We also now place a cap on the longer-term battery buildout in light of recent policy changes: utility-scale battery storage capacity gets to around 40GW by 2050, whereas it was 55GW in v3.3.

However, with lower battery CAPEX, we now augment 1h systems to 4h systems during the 2030's and see 6h BESS being built. The total GWh of battery storage is therefore similar to v3.3.

More information on this can be found here.

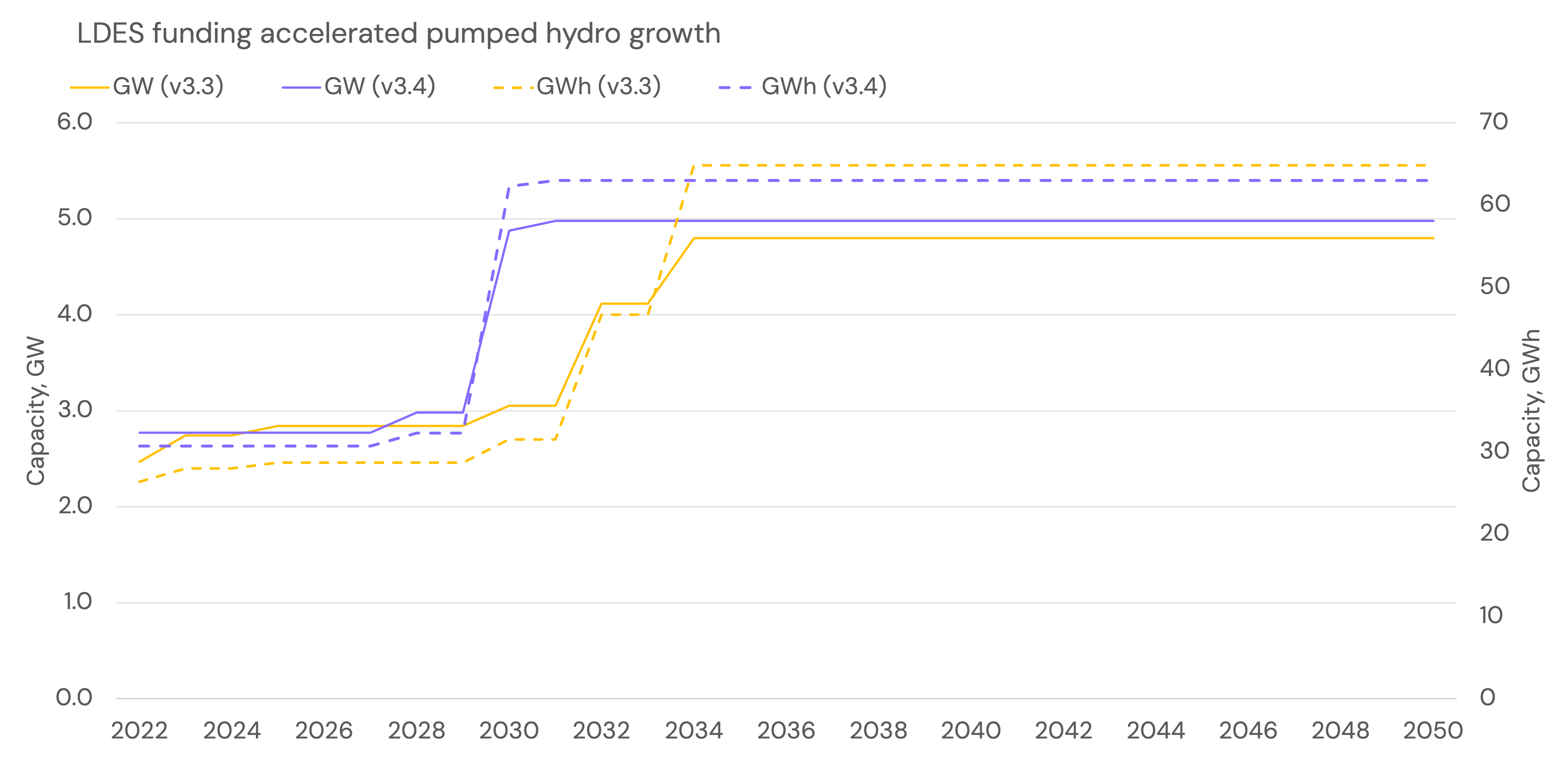

LDES funding accelerates pumped hydro build

In March 2025, the UK government announced a cap and floor scheme to support Long Duration Energy Storage (LDES) on the GB power grid. This is primarily aimed at pumped hydro.

As a result, we have updated the capacity of pumped storage as below.

New capacity additions come from Coire Glas, the Cruachan Extension, Glenmuckloch, and Glyn Rhonwy. These are pipeline sites with planning permission, a grid connection, or other consenting in place. The terms of the LDES funding state that new sites must be scheduled to deliver by 2030, and only Force Majeure events will allow commissioning dates to be pushed to 2032. We deem Force Majeure events to be very unlikely, so assume these site will come online in 2030.

Improvements to BM modelling

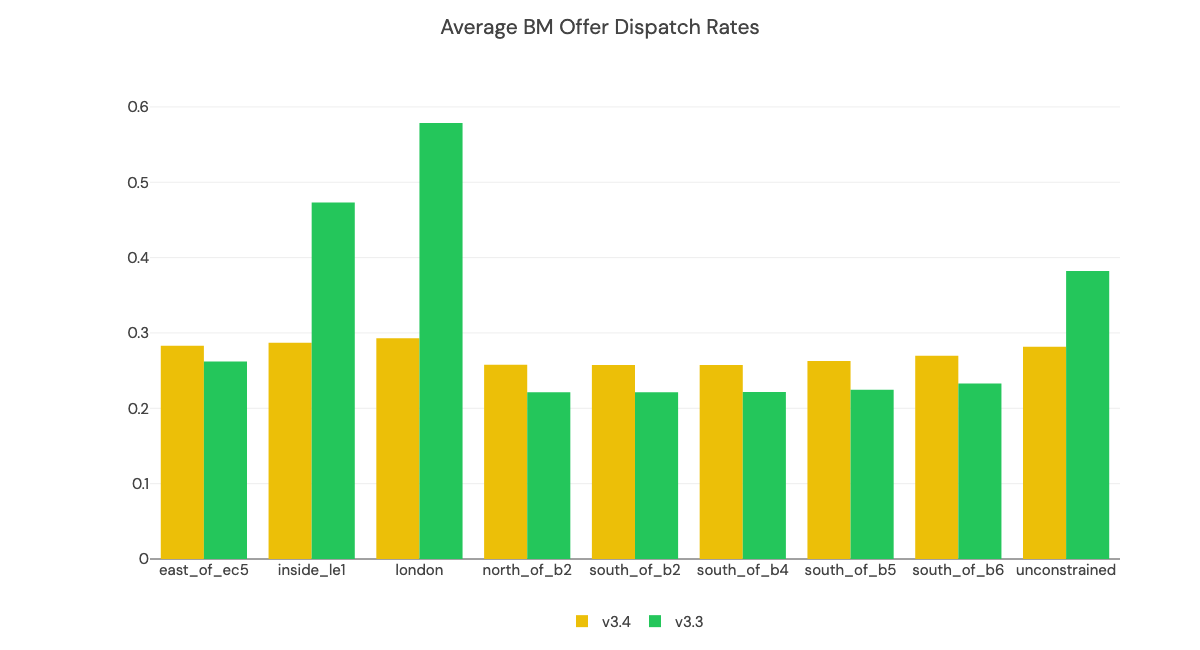

We have made various improvements to the modelling of both dispatch rates and battery operations within the Balancing Mechanism (BM):

- Updated historic battery dispatch rates with the latest observed in the market. These are blended with the forward-looking model to 2027.

- Aligned the generators that compete for BM volume with the capacity expansion logic within the model, meaning more competition from battery storage.

- Avoid double counting available generators that do system-flagged actions from those doing energy-flagged actions.

- Retrained the dataset using historical wind data, which is used to forecast the volume of energy actions.

The cumulative impact of all of these changes is to decrease dispatch rates in the Balancing Mechanism (though not for all years, for all boundaries!)

Over the last 12 months, dispatch rates for batteries in the BM have more than doubled. There is now more certainty in batteries being dispatched in the Balancing Mechanism, and we have observed different behaviours across the country of batteries using bids or offers in their trading strategies.

We now optimise battery assets in the Balancing Mechanism as the final step in the dispatch optimisation algorithm, using a linear program to decide when the system could do a bid or an offer, depending on the prices of these, and location-specific dispatch rates.

- Cycling constraints are now always respected (previously, in some years modelled cycling was a little high).

- We see greater disparity between the revenue stack in different locations, aligning better to benchmark figures in the ME GB BESS indices. We now split out rebalancing revenue/cost and offer or bid revenue/cost - so that energy rebalancing actions are attributed to Intraday revenues, rather than Balancing Mechanism revenues.

Generally, BM revenues for batteries are now lower, as a result of lower dispatch rates.

More information on all of the updates to the BM model—including refreshed documentation pages—can be found here.

Improvements to custom runs involving co-location

- We have replaced the generation profiles for solar sites, now using pvlib (previously we were using Renewables Ninja). The solar profiles are now more realistic, with more shape through the day. In addition, they can be 'more custom', requiring parameters such as tilt and azimuth, which can alter the daily profile.

- We have reviewed the logic that stitches solar profiles to our weather year. It uses a similar ranking-of-days logic that is explained here, where the sunniest days each month on a site are aligned with the sunniest days each month nationally, within the fundamentals model. This results in lower capture rates for standalone solar sites on sunny days, better reflecting reality.

- More outputs are now included in custom runs as standard - including metrics like Specific Solar Production, a breakdown of Clipped and Unclipped solar generation (MWh), Load factor (%), Solar Capture rate (%) and Solar Capture price (£/MWh).

Updated calibration to the ME BESS GB benchmark

Given recent changes in both the ME GB BESS Index (to include intraday revenues) and the Balancing Mechanism influencing trading strategies, we have updated the calibration of the GB forecast to the GB BESS Index. We now include Day-Ahead and Intraday wholesale trading, Dynamic Frequency Response services and Balancing Mechanism revenue streams.

It is now 65% in the Central Scenario, down from a previous value of 85%.

There are several reasons for the decrease in calibration value:

- The dispatch model assumes a cross-optimisation between day-ahead wholesale and frequency response revenues, and an intraday dispatch based on a rolling 2-hour window. There is further re-optimisation within the Balancing Mechanism, assuming location-dependent dispatch rates and some level of foresight of available BM revenues. This results in a highly-optimised strategy, and the percent of perfect real assets are able to achieve is lower than in a more simple market dispatch such as the day ahead trading with frequency response strategy (like the one used previously). It also captures non-physical trading between day ahead and intraday markets, and has more foresight of BM prices than previously - which we estimate account for around 15% increase in revenues.

- There is a far greater variation in performance across the battery fleet. The ME GB BESS Index uses nameplate capacity to normalise battery revenues, rather than the battery's 'current' ability to charge or discharge. It incorporates the impact of degredation across the fleet. For older, degraded assets (50% of assets by count were commissioned before 2023 and 25% of assets before 2020), this results in a lower £/MW value. In addition, due to technical (or warranty) limitations, older assets may not be able to capitalise on all the opportunities the markets present. New assets, on the other hand, should be technically better than older assets due to improvements in battery manufacturing and able to capture a higher £/MW.

- The forecast is typically applied to new assets so we now use the 75th percentile of assets to calibrate in the Central Scenario. However, combined with the latest dispatch model, find the calibration rate has fallen.